Travel restrictions for China have lifted, but industry experts remain cautious about fundraising

Travel restrictions for China have lifted, but industry experts remain cautious about fundraising

As China begins to reopen after three long years, Chinese firms are finally able to meet with foreign investors and institutions again. As of this month, passengers flying to China no longer need to do PCR tests to check for COVID-19, and countries that had previously imposed testing requirements on those arriving from the country have also lifted such rules. China has started issuing the full range of visas to foreigners.

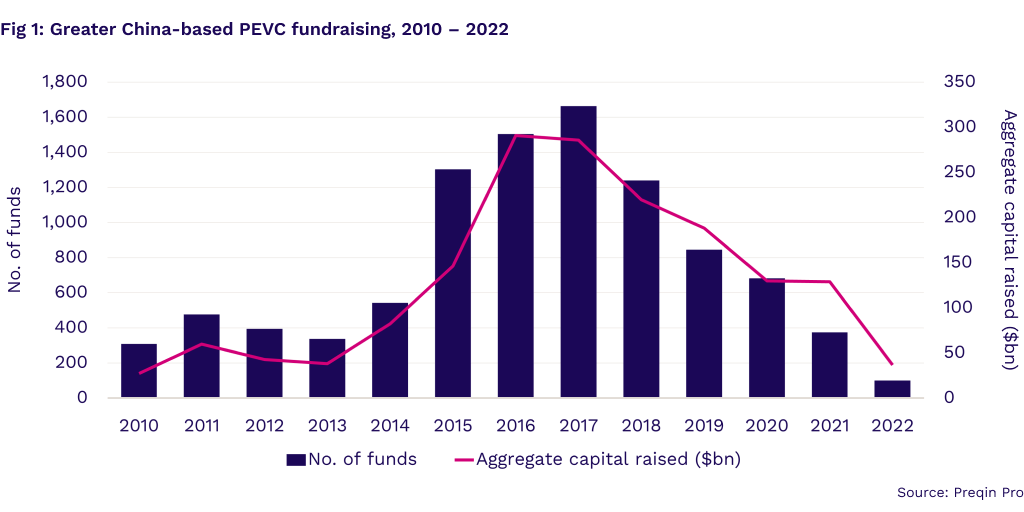

These new circumstances are welcome after such a weak fundraising year in 2022, characterized by persistent lockdowns, geopolitical tensions, and a weak economy. This heightened investor caution toward China’s private equity and venture capital (PEVC) industries, which had already been negatively impacted by regulatory changes in 2021, targeted at the edtech, property, and internet sectors. Given the tough conditions in the past few years, only 19% of respondents in the survey analyzed in our latest Investor Outlook report cited China as an appealing investment destination, down from 49% in November 2021. Aggregate capital raised by Greater China-based PEVC fund managers fell to just $36.8bn in 2022, significantly lower than the average of $148.9bn between 2019 and 2021 (Fig. 1). For a more comprehensive picture of how China’s PEVC industries have fared, read our latest Territory Guide, Private Equity and Venture Capital in Greater China 2023, also available in Chinese here.

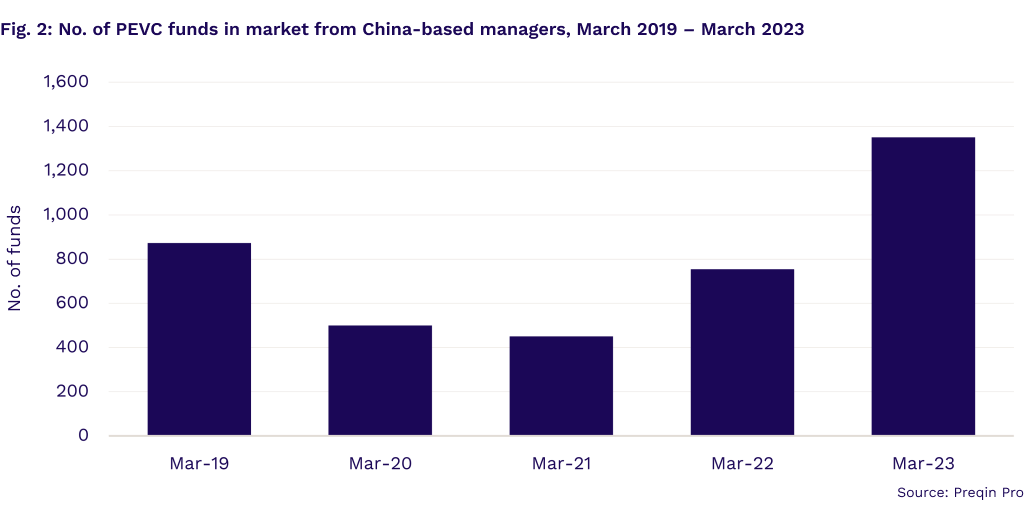

However, there are early signs of fundraising activity picking up. Currently, 1,351 China-based PEVC funds are in market – 80% more than the number of funds in market in March last year, and 3x the number of funds in market in March 2021 (Fig. 2).

While some industry players are optimistic that these developments will spur the retail, travel, and tourism sectors, as well as improve fundraising and deal-making conditions in the region, others remain more cautious.

Experts generally agree that compared with previous years, there may be more onshore funds in the near future thanks to China’s Qualified Foreign Limited Partnership (QFLP). Foreign investors can establish foreign-invested equity funds or firms onshore, with domestic or overseas investors. Most recently, private equity firm Warburg Pincus raised $439mn in its maiden yuan-denominated fund after approaching multiple Chinese investors. An RMB fund makes it easier for funds to invest in opportunities in China, but a local partner fund is required.

How else might the market outlook and investor expectations evolve for China’s PEVC industries? We spoke with five industry experts from Cowin Capital, Deloitte, MSA Capital, Hopu Investments, and Huatai Securities, to learn more about investor views on China’s reopening and its impact on PEVC fundraising there.

_______________________________________________________________________________________________

With COVID-19 restrictions lifted, we are seeing LPs from the US, Europe, and other parts of the world gearing up to make their first business trips to meet GPs in China after more than three years. Due diligence will become more feasible, and we believe LPs will be more ready to make commitments to GPs toward the second half of 2023.

However, we anticipate LP commitments to Chinese GPs will slow. Investors will reassess their investment strategy, the capability of Chinese GPs, whether they still fit the market, and whether they are still able to remain competitive in the market. Over the past few years, investment focus in China has moved from the technology, media and telecoms, and consumer sectors toward deep-tech and manufacturing, with many GPs embarking on a new process of readjusting and rebuilding their investment capability.

We should expect fundraising by RMB funds to surpass that of USD funds in 2023, because US-based LPs will need more time to justify fresh commitment to Chinese GPs as risks and concerns about China have not yet been fully mitigated.

_______________________________________________________________________________________________

We see shifts in fundraising dynamics in China. First, capital raised will be concentrated in top-tier PEVC funds. Second, government-backed industry funds and guiding funds are the major LPs of RMB funds, and are now taking a more leading role in VC rounds on key national strategic sectors such as semiconductors, new energy, artificial intelligence, robotics, aerospace, healthcare, and life sciences.

However, investors will remain cautious due to inflationary pressures, geopolitical tensions, supply chain transformations, and China’s regulatory changes. We noticed US-based LPs, particularly in retirement funds, have reduced their allocations to China. We do not foresee foreign LPs withdrawing from the Chinese market, but it will take time for them to regain confidence.

_______________________________________________________________________________________________

Today, China-focused GPs face wars on two fronts. First, they must convince global investors they can trust the governance regimes for China’s financial sectors. After three years of zero-COVID policy and regulatory interventions in the technology sector, uncertainty around offshore listings has significantly undermined investor appetite for the market. This is within the direct control of Chinese policymakers, but it could take years to rebuild investor confidence.

Second, GPs must contend with how to assuage investor fears around sustained US actions aimed at curbing China’s access to capital, talent, and critical hardware due to ongoing geopolitical brinksmanship between the world’s two largest economies. This aspect is far more volatile and intractable but may prove more smoke than fire. In most instances, the pragmatic implications of US actions are far less severe than advertised, but the halo effect can be equally destructive.

_______________________________________________________________________________________________

The ability to travel and meet companies freely will facilitate business, but the outlook is one of cautious optimism as we are not yet seeing either GPs or LPs making any significant commitments. The key concern for GPs is that private market valuations have not yet fully adjusted vis-à-vis public markets. As for LPs, we believe they are still monitoring for clearer signs of economic and regulatory robustness and sustainability.

Going forward, we believe more funds will consider onshore fundraising, as there will be increasingly more domestic companies that focus on pure domestic strategies more suited to RMB investing. Private equity players will need to consider concurrent USD and RMB strategies to have maximum flexibility to capture investment opportunities.

_______________________________________________________________________________________________

China-based investors seem less worried by the intractable denominator effect than their international peers. They have different preferences when it comes to asset allocation and rebalancing regimes, making their allocations to private equity less impacted by the poor stock market performance last year. Still, they have been relatively more cautious to commit to new funds than before.

Although fundraising challenges that emerged in 2022 will likely persist into 2023, both RMB and USD funds should pick up as China reopens, particularly if what is now happening in Hong Kong is any indication. Moreover, we may expect to see lower interest in China GPs’ USD-denominated funds from US investors, compared with an increase in the Southeast Asia and the Middle East and North Africa regions.

Commentary in this article is provided by experts from the Preqin Expert Voices network.

Preqin Expert Voices is a global network of alternative asset professionals with in-depth industry knowledge and valuable ideas to share. We invite senior leaders and highly experienced commentators from across the industry to share their opinions in our forum, including fund managers, investors, consultants, advisors, academics, and more.

Are you a senior executive or thought leader? Are you a regular industry speaker? Are you a frequent commentator in the press? If this sounds like you and you would like to become an Expert Voice, then please get in touch at expertvoices@preqin.com.