More than 22% of buyout deals in North America in 2020 passed the $1bn threshold

More than 22% of buyout deals in North America in 2020 passed the $1bn threshold

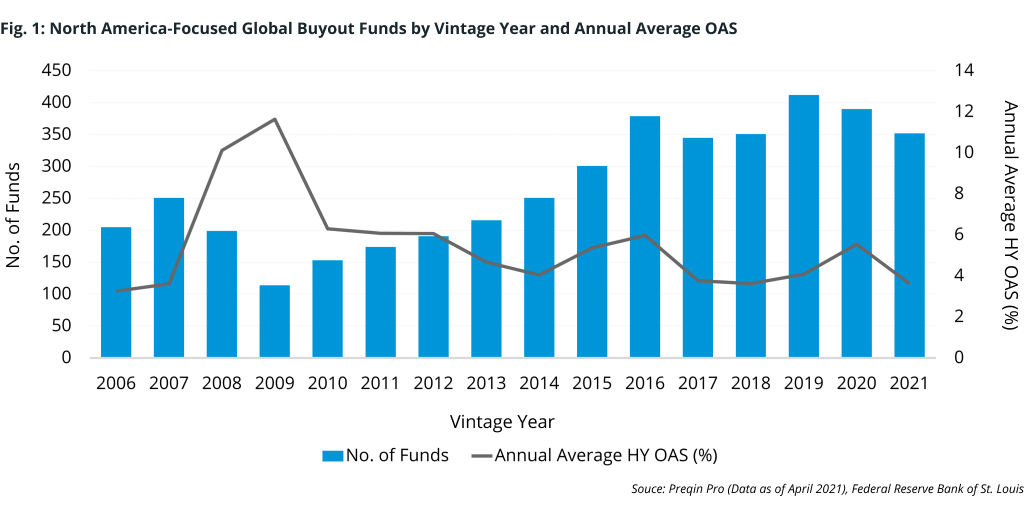

The low-yield environment following the Global Financial Crisis created fertile ground for private equity buyout funds. Between 2010 and 2016, the North America-focused buyout fundraising market grew by an average of 37 per year, eventually peaking at 412 funds closed or raising capital in the 2019 vintage year (Fig. 1). Rapidly increasing demand for these strategies, fueled by their strong performance in a landscape characterized by yield-starved investors, created a risk-on trend of ever-larger deal-making.

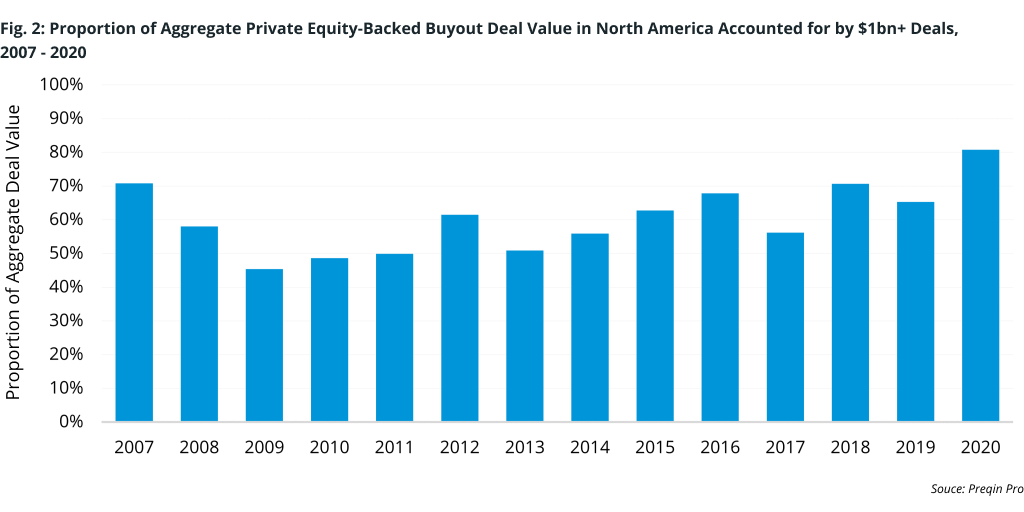

Yield spreads, measured here as the option-adjusted spread (OAS) of high-yield bonds to the 10-year US Treasury, fell from crisis highs to below 6%, and even 4% over some stretches of time, meaning borrowing came cheap for deal-makers. What followed was a larger proportion of North American buyout deals valued at more than $1bn. In 2011, about 11% of buyout deals crossed the $1bn threshold; in 2020, that figure was greater than 22%. By value, these mega deals accounted for more than 80% of activity in the world’s largest buyout market, up from 65% in 2019 and the largest proportion yet (Fig. 2).

Catalysts for this growth are likely a combination of the influx of capital into private equity managers and the consequential effect of attracting new funds to market. Global private equity assets topped $6tn as of September 2020, with buyout funds making up about $2.42tn of that, including a record level of dry powder. Further distilling that total, $1.46tn of those buyout assets are focused on North American markets.

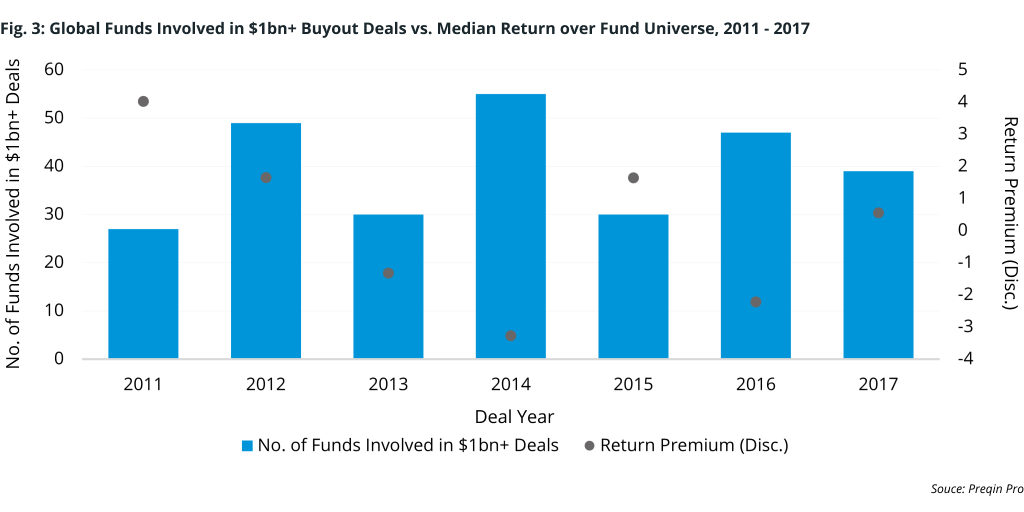

As transaction sizes grow, questions of a winners’ curse arise. Are some deals creating bidding wars that end in the winner holding an overpriced asset? Evidence suggests that funds involved in these larger deals have struggled to outperform the median IRR of funds not involved in these deals (Fig. 3). Additionally, PrEQIn Index data shows that small- and middle-market buyout funds outperform large-market funds more than 70% of the time on a rolling one-year basis.

What does this mean for investors? It highlights the importance of due diligence. LPs, and their consultants, need to ask managers and prospective managers how they price their deals and at what point they would walk away if the bidding gets too high. The small and middle markets have historically done so, and by their nature been high-risk, high-reward asset tiers. However, the trade-off with larger markets’ risk/return relationship could become more asymmetric if deal multiples and debt loads rise beyond what a portfolio company is realistically capable of delivering.