Equity valuations and low yields from fixed-income investments are set to boost alternatives allocations, driving significant growth

Equity valuations and low yields from fixed-income investments are set to boost alternatives allocations, driving significant growth

The alternative assets market has grown significantly in recent years, and Preqin expects assets under management (AUM) to reach $10.74tn at the end of 2020. Our AUM forecasts show alternatives rising to $17.16tn at the end of 2025, but are there limits to the size of the market? We would argue not.

Alternative assets are generally an important part of a wider multi-asset portfolio, performing a vital role in the balance of risk and return. The illiquid nature of most alternative assets can act as a counterweight to listed equity and tradable fixed-income portfolios, which can balance cash flow needs within a portfolio due to their liquid nature and can reprice quickly. This creates a real-time view for investors, which is not always reflected in their alternative assets investments given the way they are valued. Without immediate revaluation, private assets can smooth volatility, as we have seen with some assets during 2020.

The Interest Rates Effect

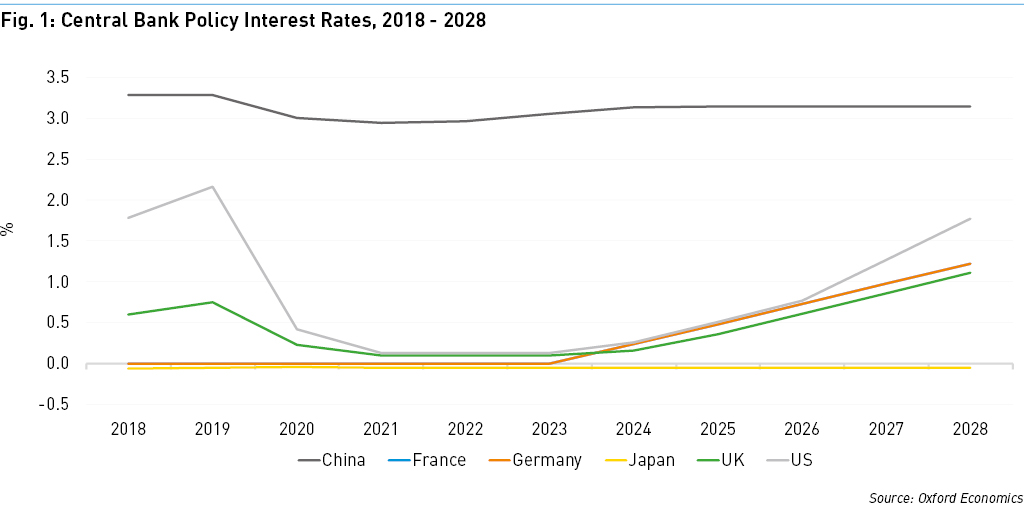

Allocations to alternative assets are a key driver of market growth. The outlook for the next several years appears to be a further period of low or negative real interest rates across major economies. Central bank policy rates in the major developed economies of the US, Japan, Germany, France, and the UK are expected to remain below 0.5% through to 2025, according to Oxford Economics (Fig. 1).

This is pushing investors to seek either alternative sources of yield or new sources of growth, given the speed of the equity recovery during Q2 and Q3 2020. The S&P 500 trades on a forward P/E of 20.9X estimates for calendar year 2021, compared with an average of 20.5X for 2016-2020F¹. It could be argued that at this point in the cycle, with so much uncertainty, equity markets are aggressively valued.

The combined forces of high equity valuations and negative yields from many government bonds are expected to push more investors toward alternative assets. In a recent investor presentation Brookfield Asset Management argued that allocations to alternatives could increase from 25% in 2019 to 60% in 2030. If this came to pass, AUM would surge from existing levels.

When valuations are solid, equity markets play a significant role in exits, allowing capital to be recycled. Preqin data in Q3 2020 highlighted a significant increase in the number of exits via IPO across the venture capital industry, which helped push exit valuations to a new quarterly record of $118bn. Trade sales also have a very important role to play and still dominate exits across alternative assets markets, including venture capital, with high valuations making it easier for listed acquirors to pay top dollar.

The Benefits of Oversight

Throughout 2020, one major benefit of private equity ownership has been the close relationship between managers and portfolio companies, with direct reporting lines between executives and shareholders and access to far more detailed financial performance numbers than listed companies disclose to their investors. Operating through times of crisis has proven the model can work in the most difficult of economic environments, which may alleviate concerns among potential investors about the strength of leveraged investee companies.

With a wide range of drivers for future growth in the alternative assets market and several potential ways in which participants can deploy and redistribute capital, there appears to be few obstacles in private capital’s path to future growth as a major asset class that complements public capital markets.

Download a data pack containing all the charts in our regional articles for Future of Alternatives 2025. For more predictions and projections on the future of the alternatives industry, visit Preqin's Future of Alternatives 2025 Content Hub.

¹ Source: FactSet as of 9 October 2020