Ali Javaheri

|

Hedge funds stand to gain significantly from mass-risk events as investors look to counter market volatility

Hedge funds stand to gain significantly from mass-risk events as investors look to counter market volatility

The COVID-19 pandemic is still ongoing in many parts of the world, with the now-dominant Delta variant delaying its end and the resultant supply chain bottlenecks increasing fears of inflation. Accordingly, investors will seek to further reduce portfolio risk, meaning hedge funds are expected to become increasingly crucial. At the end of 2020, 64% of managers surveyed by Preqin told us that hedge fund assets under management will increase further in 2021.

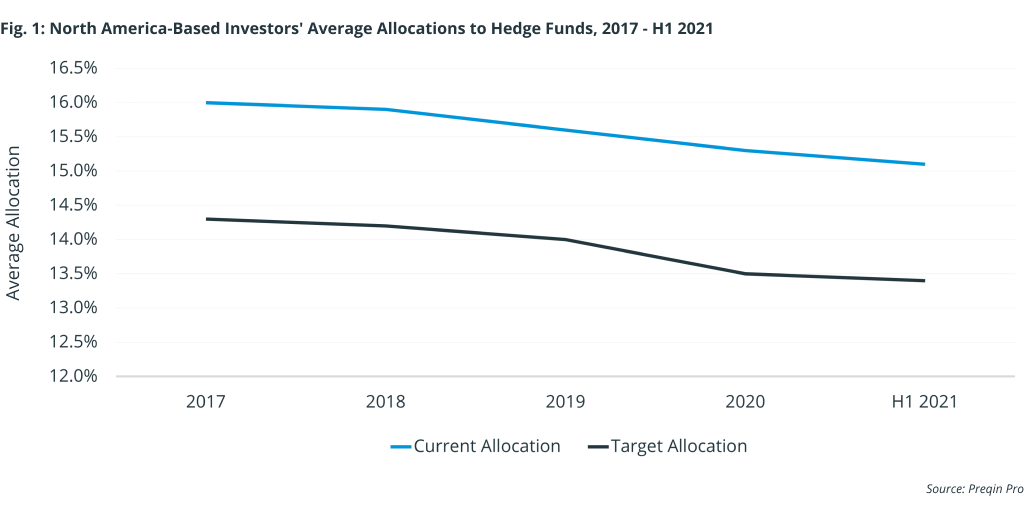

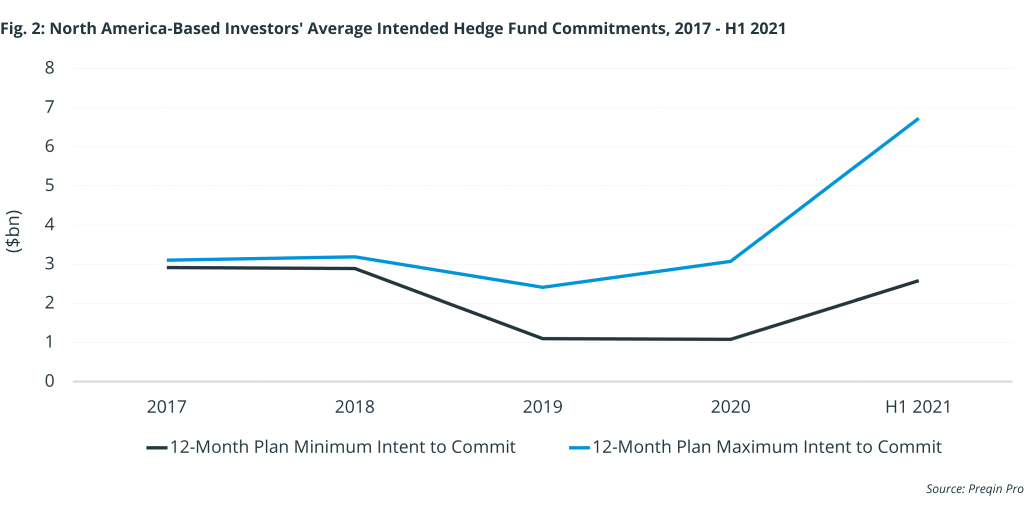

North America-based investors have increased planned commitments over the 2020-2021 period, reversing a previous downward trend (Fig. 2). This is to be expected, as historically allocations have trended upwards following economic downturns. If these commitment ambitions are met, it will lend further credence to the notion that investors are allocating more money to hedge funds to reduce the risk inherent in a volatile equity market.

Given that hedge funds had experienced consistent net outflows in the years running up to the pandemic, what has changed investors’ minds? The past 18 months or so of market turmoil have reminded everyone that hedge funds can materially lower portfolio risk and help insulate capital from significant losses. Over the past decade, the average down-quarter return for Preqin’s All-Strategies Hedge Fund Benchmark outperformed the MSCI World TR Index by 4.95%, and the S&P 500 TR Index by 4.78%. As expected, and by design, hedge funds underperformed the indices in up markets by 2.18% (MSCI World TR) and 2.99% (S&P 500 TR Index).

But that’s just half the story. What’s more is that over rolling three-year periods, the standard deviation, or risk, of Preqin’s hedge fund index was about half of global and US large-cap public equities. For investors hoping to manage portfolio risk, as most institutional investors are, hedge fund allocations can help get them there – lower-risk investments will lower portfolio risk.

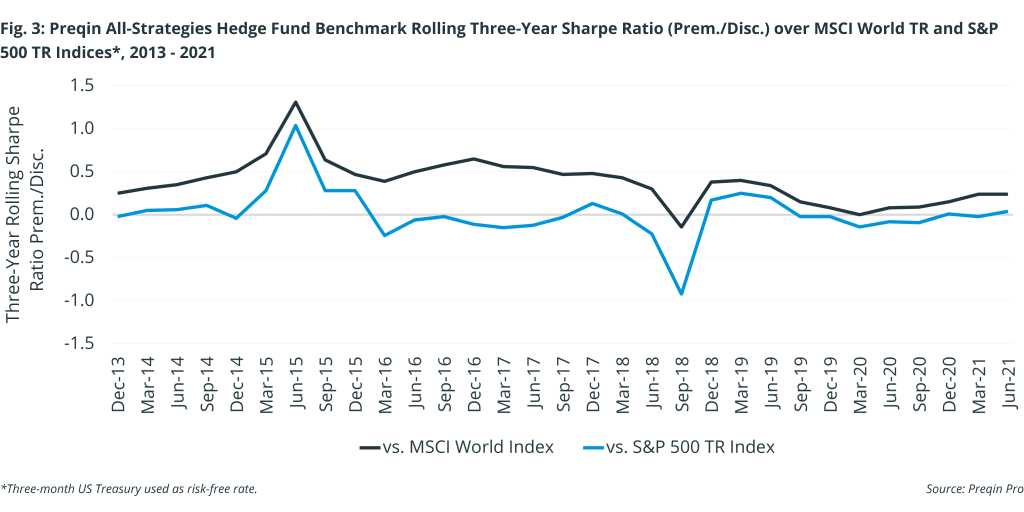

Addressing the trade-off between lower risk vs. lower returns, the Sharpe Ratio weds the two. Hedge funds, by way of Preqin’s All-Strategies Hedge Fund Benchmark, showed superior performance to global equities (MSCI World TR), but with mixed results relative to US equities (S&P 500 TR) over rolling three-year periods in the past decade (Fig. 3).

The argument can certainly be made for US large caps over hedge funds. Risk, measured by quarterly three-year standard deviation, has been nearly double that of hedge funds at times, but strong returns have made up for that trade-off. However, the COVID pandemic has proven that hedge funds can insulate portfolios from the drawdown. Hedge funds caught only about half of the downside of US equities’ Q1 2020 drop – at -10.4% vs. -19.6% respectively – and while their rebound was lower than that seen in US equities, the net performance over the period was better.

Consequently, investors may have determined, at least for the time being, that the high-risk macroeconomic environment jeopardizes portfolio returns, and hedge fund allocations can increase predictability and therefore increase returns. Going forward, more mass-risk events – be they climate disasters, pandemics, or political unrest – could further boost allocations to hedge funds, and perhaps permanently so.