The aggregate value of PERE deals in the US fell by 68% in Q2 2020 from the previous quarter – with every sector recording a decline

The aggregate value of PERE deals in the US fell by 68% in Q2 2020 from the previous quarter – with every sector recording a decline

Every sector of real estate investment across the US has been impacted by the COVID-19 pandemic. Domestic and international travel restrictions have created cash flow issues for the hotel sector, and brick-and-mortar retail activity has declined as Americans isolate at home. With consumers turning to e-commerce more than ever before, the logistics sector has been put under strain. Meanwhile, the shift to working from home for many businesses has created questions around how office spaces may change in the ‘new normal.’

Not only has this rapid change created uncertainty in the market, but the social distancing measures and travel restrictions imposed have also made deal-making a practical challenge for real estate professionals. Indeed, 59% of alternative assets fund managers reported to Preqin in April 2020 that COVID-19 has had a negative impact on deal origination. In the face of disrupted cash flows, shifting sector dynamics, and practical challenges to business operations, private equity real estate (PERE) deal activity in the US slowed dramatically.

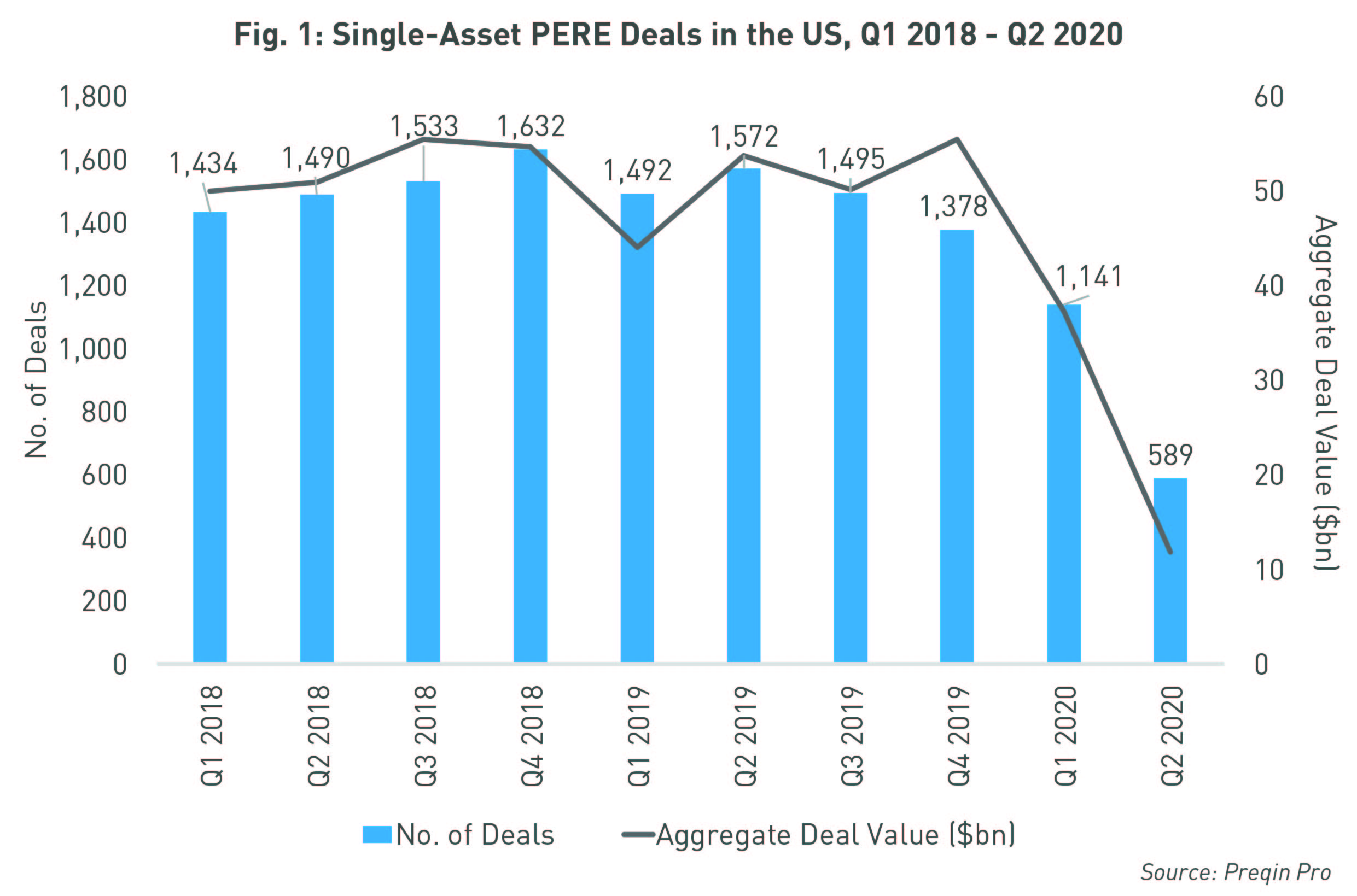

Preqin data shows the magnitude of COVID-19’s impact on the US PERE deals market so far. In each of 2018 and 2019, single-asset PERE deals in the country amounted to at least $200bn. At the midpoint of 2020, by comparison, this total stands at only $49bn. Activity in the first quarter of the year was relatively strong – the $37bn in single-asset deals fell just shy of the $44bn recorded in Q1 2019, likely explained by the completion of several longer-term transactions. But in Q2, as strict social distancing measures came into place, activity took a nosedive, amounting to only $12bn (Fig. 1).

Hospitality Sector in Freefall

Within US real estate, disruption has perhaps been most keenly felt in the hospitality sector. Following the US Government’s decision in March to largely shut down international travel into the US, cash flow in the hotel sector has been severely disrupted. Also in March, President Trump signed the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) to stimulate the economy, with some provisions – such as small business loans and payroll tax credits – directly applicable to real estate businesses. As an example, businesses in the hospitality sector with 500 or fewer employees are able to use these loans to cover rent payment, helping GPs to continue to collect rental income from these tenants.

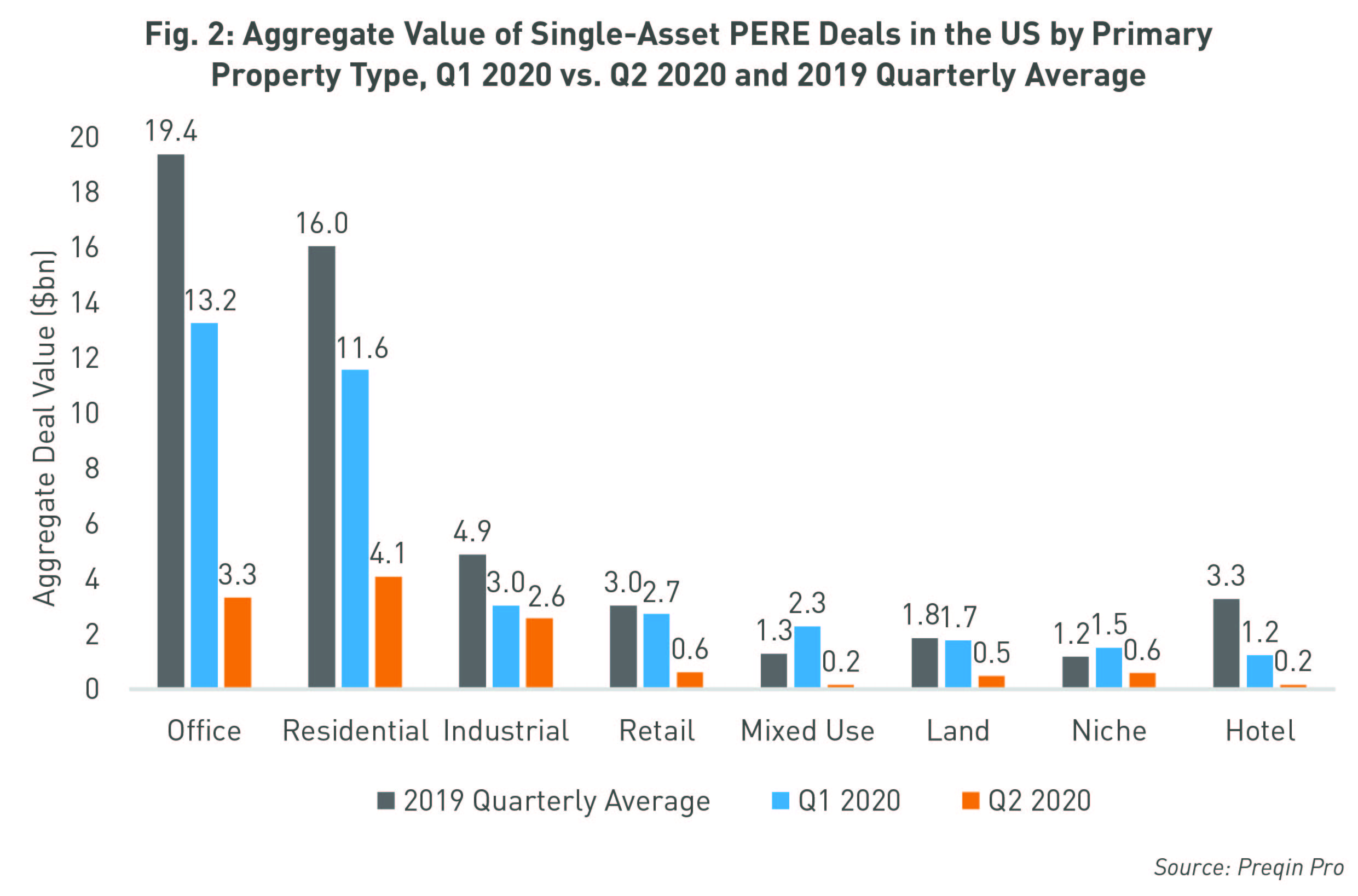

Preqin recorded just three PERE deals completed for US hotels in Q2 2020, worth an aggregate $167bn. And only $1.2bn was invested in the hotel sector in Q1, which equals roughly one-third of the 2019 quarterly average ($3.3bn). Given the uncertainty surrounding the length of the US travel ban, and the time required for the market to rebound, we expect activity to remain muted for some time.

Retail Real Estate Severely Disrupted

Brick-and-mortar retail real estate – already facing the rise of Amazon and e-commerce generally prior to the pandemic – has also been particularly impacted. With a large proportion of the US population confined to their homes, the retail sector has fallen foul of a fresh drive into online shopping. Aggregate Q1 2020 deal volume in the sector stood at $2.7bn, which is in line with the 2019 quarterly average ($3.0bn). But, in a similar trend to the hotel market, Q2 activity was minimal, recording just $0.6bn in retail PERE investment.

We expect reduced activity in this sector to continue. As more firms turn to e-commerce in a bid to maintain some level of cash flow throughout the pandemic, brick-and-mortar retail will remain under pressure. Indeed, Preqin’s survey of over 100 investors conducted in April 2020 indicated that 34% of investors are looking to avoid retail-focused real estate in 2020 following the outbreak of COVID-19.

Logistics Keeps the Momentum Going

The dramatic uptick in online shopping and deliveries may have been to the detriment of brick-and-mortar retail, but has conversely raised the attractiveness of investment opportunities in industrial and logistics assets.

Of all sectors, PERE deal flow in the logistics market has perhaps been the most consistent with recent averages since the pandemic hit. While below the 2019 quarterly average ($4.9bn), the $3.0bn of industrial PERE deals recorded in Q1 2020, and $2.6bn in Q2, highlights the continued appetite for warehousing and logistics infrastructure assets. One of the largest industrial deals completed in Q2 was Preylock Real Estate Holdings’ $110mn acquisition of Las Vegas-based Tropical Distribution Center 1. The 855,000 sqft distribution center is 100% leased to Amazon.

COVID-19 has both increased the need for efficient distribution systems, as well as accelerated the rise of e-commerce. Although deal activity would have been impacted by practical business challenges as in other sectors, we expect logistics assets to continue attracting significant investment.

Established Markets Slide, but Should Recover

Office and residential – traditionally the largest sectors for private real estate investment in the US –have seen muted activity thus far in 2020. Aggregate deal value in each sector declined by roughly one-third in Q1 2020 from the 2019 quarterly average, with activity declining even more significantly in Q2 2020 (Fig. 2).

With many businesses forced to work from home during the peak of the pandemic, investment professionals will be keen to understand how office space may be used in a post-COVID-19 world. Will workforces demand more geographical flexibility? And will office space need to change to accommodate this? US office vacancy rates recorded a 20 bps increase to 12.3% in Q1 2020, CBRE reported, but the market remains stable and likely to rebound. While remote working will likely be more common than pre-pandemic, we expect the office will remain at the core of a company’s collaboration and productivity.

Although deal flow has slowed in every sector, residential has registered the most activity in Q2. The $4.1bn of single-asset PERE deals eclipses that of the office sector ($3.3bn). Activity has been driven by several acquisitions of multi-family assets across the US. These include the $154mn sale of Cityfront Place, a 39-story high rise located along the Chicago River with views of Lake Michigan; and Pacific Urban Residential’s $108mn acquisition of Skyline Terrace Apartments, a 138-unit apartment complex in Burlingame, California. Multi-family property investment is often viewed as a defensive, cyclically resilient play, and amid the current market uncertainty the sector is still attracting capital.

A Quiet Q3?

So far in 2020, maintaining operations has proved a sizable challenge for investment professionals. Add to that the need to understand the impact of seismic shifts in sector dynamics, as well as analyzing the role that property will play in the ‘new normal’ that COVID-19 is shaping, and the industry has been significantly stretched. PERE deal activity across the US will therefore likely remain quiet throughout Q3; we expect a select amount of transactions to take place in a disrupted and socially distanced market. But with North America-focused real estate dry powder standing at a record $204bn as of July 2020, capital should begin to flow back into the market as restrictions are eased.

This article is the second in a series analyzing the impact of COVID-19 on the private real estate market, produced in collaboration with our partner EisnerAmper. We discuss deals, fundraising, and other key trends in the industry.

To ensure you don’t miss the next instalment in this series, sign up for Preqin’s weekly newsletter here.

For more insights and analysis on the impact of the pandemic on alternative assets, take a look at our COVID-19 Knowledge Hub.