High-quality mid-market firms are witnessing a surge in deal flow buoyed by record levels of dry powder amid a spotlight on valuations and tighter financial conditions

High-quality mid-market firms are witnessing a surge in deal flow, buoyed by record levels of dry powder amid a spotlight on valuations and tighter financial conditions.

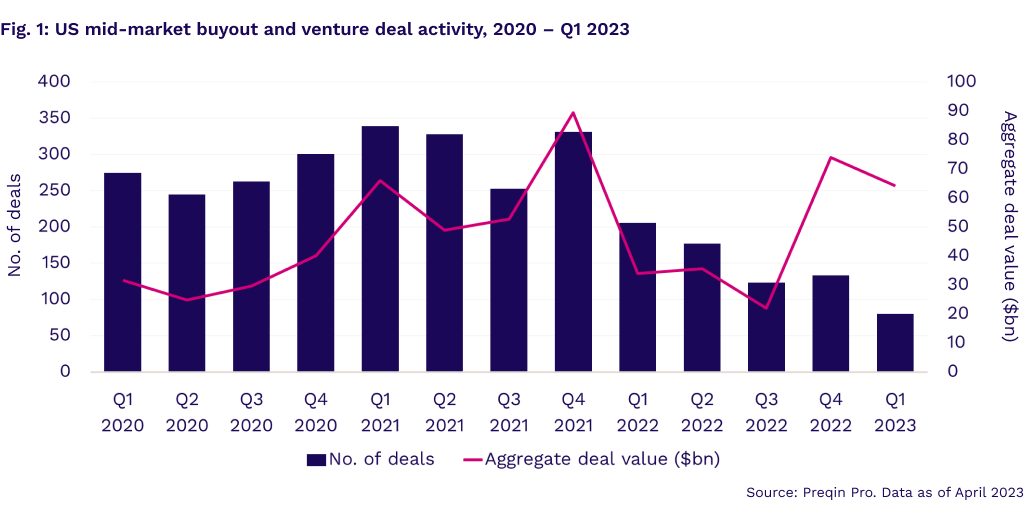

After an historic run of US middle-market deal activity in 2021, the market cooled considerably last year as dealmakers pressed pause amid uncertainties brought about by rising inflation, aggressive rate hikes, and valuation volatility. However, deal activity picked up over the last two quarters, reflecting the growing quality of middle-market companies in the US.

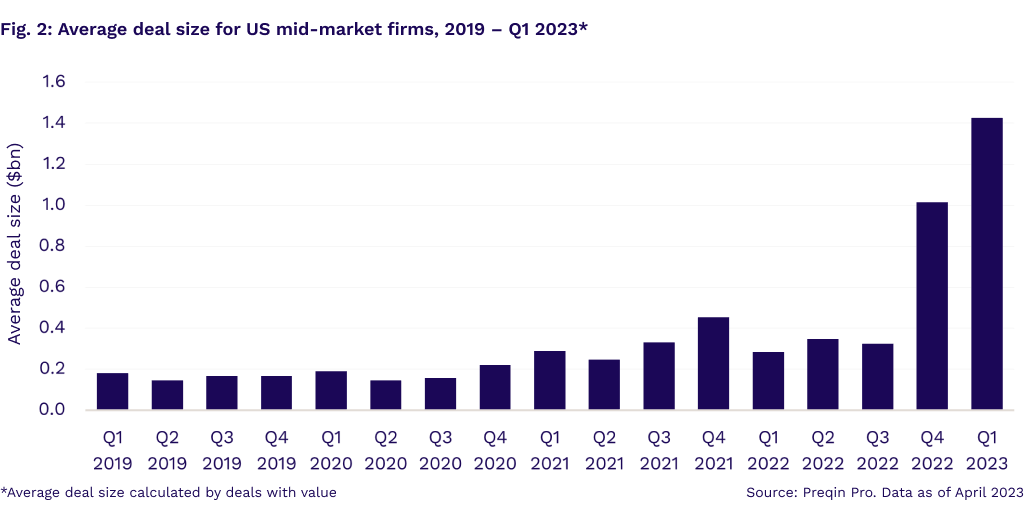

The aggregate value of US mid-market buyouts and venture capital (VC) deals surged in the fourth quarter of 2022, up 237% compared with the previous quarter to reach $74.1bn. This marks the second-best quarterly performance in the last decade (Fig. 1). The momentum carried over into the first quarter of 2023, with an aggregate deal value of $64.2bn across 80 deals. Despite being the lowest deal volume in a decade, the high aggregate deal value meant that average deal size hit an historic high of $1.4bn, surpassing the previous quarter’s record of $1bn (Fig. 2).

Much of this is likely due to private equity and venture firms sitting on record levels of dry powder. As of April 2023, that surpassed $2.5tn for the first time, according to Preqin Pro data. This meant they had an unprecedented amount of cash to deploy. As shown in the 10 mid-market deals worth over $1bn in the US this year, eight were all-cash transactions. In the case of Qualtrics, less than 10% of its financing came from debt when it was taken private, while the acquisition of Immucor was financed through a combination of cash and debt, although the specific details remain undisclosed.

What's more, leveraged buyouts in large caps are becoming more expensive. This is because borrowing costs are higher as rates rise, and there is a valuation mismatch between buyers and sellers. Both factors have pushed private equity and venture firms toward the mid-market in search of deals that are easier to finance and execute. Although the number of deals has decreased, indicating dealmakers’ cautious stance, the significant aggregate transaction value suggests they remain prepared to pay for worthy deals.

Amid economic uncertainty in the current market climate, mid-market deal activity has proven more resilient than larger deals. This is in part due to a lower reliance on debt financing for leverage and wider and more fluid exit windows, given the current weak IPO market.

Billion-dollar mega-buyouts

While deal sizes are shrinking in large-cap companies, at least 10 mid-market deals were valued at over $1bn each in the first quarter of this year alone. The volume of these megadeals almost matched 2022’s 13 deals worth over $1bn each. Qualtrics’ $12.5bn take-private deal by tech-focused private equity firm Silver Lake emerged as one of the largest private equity buyouts across all categories this year, reflecting strong investor confidence in the mid-market segment.

According to the Golub Capital Altman Index (GCAI), which monitors around 110−150 US mid-market businesses backed by private equity, these companies experienced an 11% year-on-year increase in earnings and revenue growth during the first two months of the year, surpassing expectations. The results suggest that the tailwind of falling energy prices more than offset the headwind of rising interest rates, helping to boost consumer confidence and profit margins.

With improving business prospects alongside lower valuations, mid-market companies have become more attractive to investors. These smaller companies are typically recognized for promising growth potential in both scale and operations, which could mean that operational improvements cause earnings to grow.

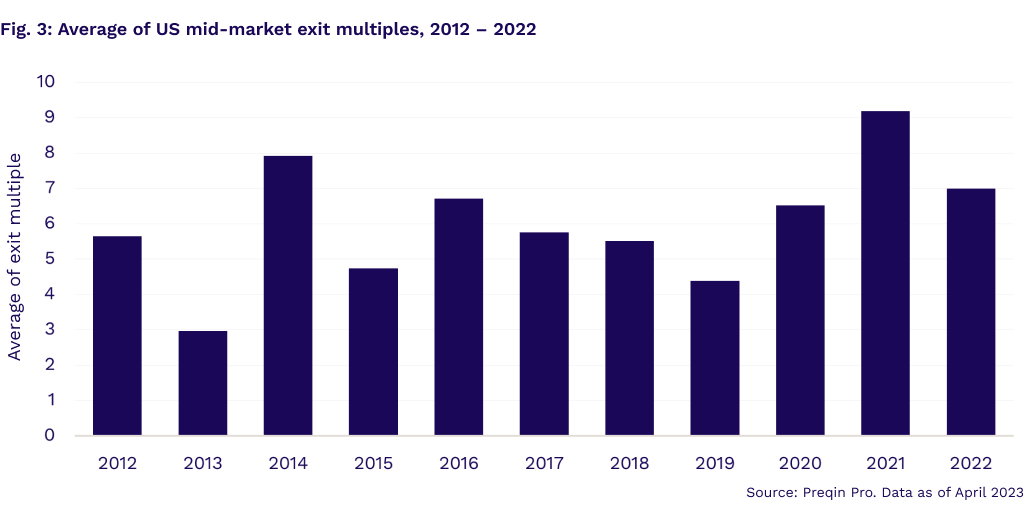

The exit environment in the US mid-market sector has been robust, hitting an all-time high exit multiple of 9.18 in 2021, the most active year for deals over the past decade. Although the exit multiple fell to 7 in 2022, it was still above the 10-year average of 6.25x, indicating healthy returns for investors (Fig. 3).