Singapore-based LPs share their top concerns when considering investing in Japanese VC, a young but fast-growing industry

Singapore-based LPs share their top concerns when considering investing in Japanese VC, a young but fast-growing industry

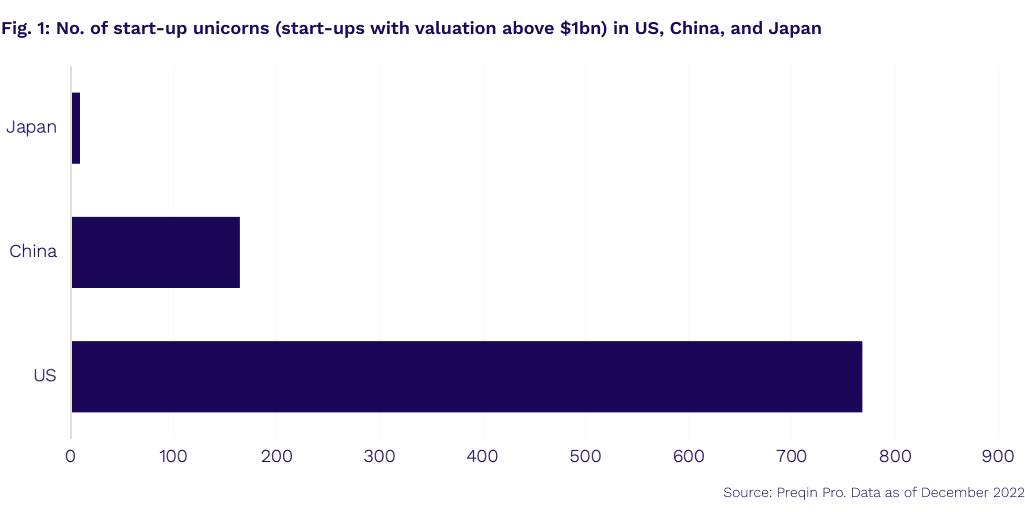

Despite the large strides taken by its government and industry players, Japan’s venture capital (VC) scene is still emerging. Foreign LP participation is very low at only 0.8%, compared to over 20% in the US. The third-largest economy is home to just nine active unicorns (start-ups with a valuation over $1bn) that are unlisted, compared to over 700 in the US and 164 in China (Fig. 1), according to Preqin Pro.

If LPs’ criteria for investing is purely based on performance, Japanese VC appears attractive. Net IRR (%) was consistently between 10% and 18% for funds of vintages 2014 to 2017, according to the Preqin-JVCA Performance Benchmark Update for Japanese Venture Capital 2022. Funds of vintage year 2018 dipped to 7.7%. Still, Japanese VC funds demonstrate the ability to generate returns.

Why is foreign LP participation still low? Last month, representatives of Japan Venture Capital Association (JVCA) and selected Japanese VC fund managers met with Singapore-based LPs in a new outreach initiative to increase foreign LP participation in Japan’s VC industry. Shinichiro Shiraki, Head of LP Relations at JVCA and CEO of Aizawa Asset Management, said: “We chose Singapore because it is a financial hub in Asia. In our opinion, it is the best place to disseminate information on Japan VC and confirm the investment needs of institutional investors based in Asia.”

During the sessions, LPs shared a common sentiment that Japan VC is a relatively closed market that they’ve not had much exposure to. As a result, they said it’ll take some time for them to understand the market and where the opportunities are.

Below we’ve listed some common questions asked by the LPs.

1. Why has there been low foreign LP participation for so long?

One reason for the predominance of domestic LPs is that there’s a language barrier, as the reporting structure and administrative tasks are usually conducted in Japanese. This, coupled with the fact that the talent pool for VC is smaller, with fewer investor relations staff, and even fewer English-speaking ones, make it challenging to promote funds.

However, Japan is demonstrating signs of an expanding talent pool. Senior executives of corporate venture capital (CVC) funds have gone on to establish their own independent VC funds. For instance, previous senior management executives of CyberAgent Ventures (a CVC spinoff from Japanese internet media company CyberAgent) have established their own independent VC firms.

Previously dominated by CVC firms and domestic LPs, the landscape of Japanese VC is changing.

2. What’s the typical ticket and deal size in Japan?

While LPs at the session were keen on early-stage investments, they said that small ticket sizes can be a barrier. Institutional investors typically commit to funds of a certain size, which will have correspondingly larger ticket sizes. Some LPs aim for a minimum ticket size and a maximum allocation of the total fund.

VC opportunities in Japan are now more abundant in the early stages. Valuation for companies at the seed financing stage are typically around $1mn to $5mn, whereas those raising Series A capital could be valued at between $8mn and $15mn.

However, lower ticket sizes also mean that Japanese companies are typically listed at relatively lower valuations compared to the US, which makes it easier for investors to exit.

3. Which sectors feature prominently in portfolios?

LPs were most curious about the sectors receiving the most VC investments in Japan. The Japanese GPs said that they’re seeking to ride the wave of government support to invest in Japan’s content (animation and manga), artificial intelligence, semiconductor, energy, and robotics industries.

With an aging and shrinking population, digital transformation is sorely needed in traditional industries such as finance, manufacturing, construction, and real estate in Japan. While there has been a boom in the number of Software as a Service (SaaS) start-ups, there is still room to enter the market. SaaS has applications across nearly all B2B businesses, which contrasts with the fintech payment sector, where mainstream payment fintech is already dominated by some of the largest companies, and success depends on whether there is a real niche.

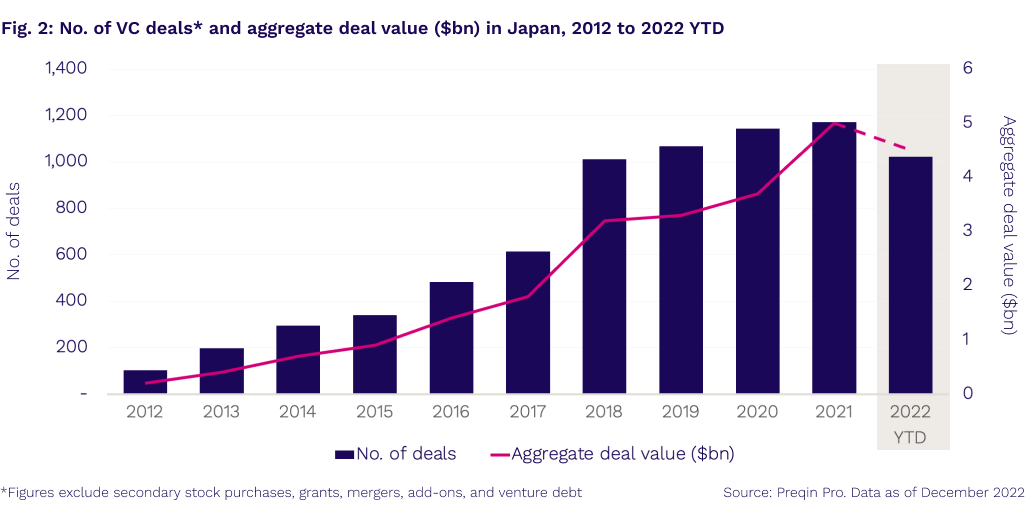

According to Preqin Pro, among the 1,023 VC deals with an aggregate deal value of $4.5bn concluded year to date (Fig. 2), over 20% are in the SaaS vertical, across various industries such as healthcare, financial services, and business support services.

One GP also said that buy-now-pay-later and micro-credit start-ups that evaluate loan applications based on dynamic data, rather than static data like annual income, will see higher demand. Examples of such services include China-based WeChat and Alipay.

With digital transformation driving the market, re-skilling start-ups in the post-pandemic era becomes increasingly important. Edtech start-ups focused on this area could also see significant opportunities for growth.

To attract more foreign LPs, there needs to be increased awareness and education on how to operate in Japan. Domestic GPs also need to understand the needs and priorities of foreign investors. JVCA’s Shiraki said: “In the future, we will create opportunities to communicate to domestic and foreign institutional investors about the promise and attractiveness of start-up investment and VC assets in Japan.”

Indeed, the VC market is maturing. Japan’s Government Pension Investment Fund’s first commitment to a VC fund this year, coupled with the weaker yen, will continue to add to the industry’s attractiveness. Read more about Japanese VC in our territory guide.

Power your deal-making with accurate and comprehensive private market data and intelligence on investor-backed companies. Get a complete view of the private capital lifecycle with interconnected company, fund and performance data. Find out more about Company Intelligence today.