Japan has experienced a pick-up in deal interest among notable foreign private equity houses in recent years, but highly anticipated value creation opportunities have been challenging to realize – will 2021 be the start of improved traction?

Japan has experienced a pick-up in deal interest among notable foreign private equity houses in recent years, but highly anticipated value creation opportunities have been challenging to realize – will 2021 be the start of improved traction?

The Land of the Rising Sun has weathered the pandemic-induced crisis relatively well. In Q4 2020, real GDP was down a mere 1.2% from a year earlier, boosted by a strong recovery in consumer spending, ample foreign demand, and robust fiscal stimulus measures implemented by the government. In comparison, real GDP in the US and EU was down 2.4% and 4.8% respectively. While a steady rise in COVID-19 cases in Q1 2021 could put a short-term damper on improving domestic consumer demand, Japan’s public health system’s response thus far has been reassuring. Indeed, the long-term economic prospects and investment case for the country remain positive.

For the private equity industry, attention is shifting to look beyond the pandemic back toward long-held structural issues. A sustainable recovery will depend on addressing Japan’s rapidly aging population, enhancing labor force productivity, and unlocking pent-up value in domestic corporations weighed down by clumsy governance structures. Despite being one of the most advanced economies in the world there is a long way to go to lift the country’s industrial competitiveness on the world stage. GDP per capita is 19% lower than the top half of OECD countries, while labor productivity is 28% lower than these best performers. However, these factors present an opportunity for patient capital willing to tap into succession challenges, embrace digitalization, and untangle spools of red tape.

Deal Activity: Strongest Q1 in Three Years

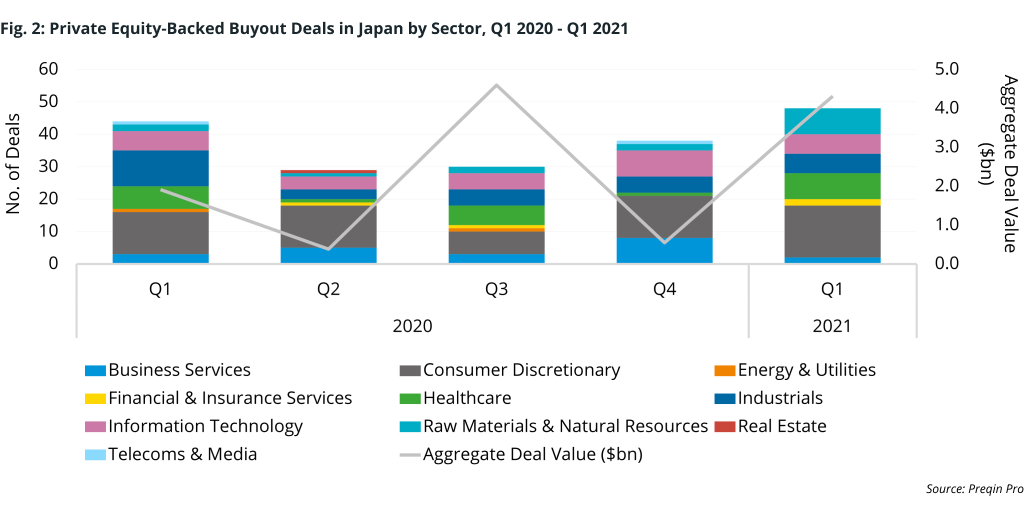

The onset of COVID-19 brought with it a rise in uncertainty for private equity deal-makers, but has also highlighted the increasing need for private capital in driving competitive transformation in Japan. Instead of shying away from new investments, deal activity in the buyout market has held strong over the last year. In 2020, 141 private equity-backed buyout transactions were completed with a combined valuation of $7.4bn (Fig. 2), according to Preqin Pro. This is on par with 2019 figures, after removing the one-off effects of the $12bn growth capital reorganization of Toshiba Memory Corporation spin-off Kioxia Holdings backed by the Development Bank of Japan (DBJ) – the largest private deal in Japan ever tracked by Preqin. 2021 looks set to be even stronger, with 47 buyout deals already changing hands at an aggregate deal value of $4.3bn in Q1. To put this into perspective, the total deal value secured in Q1 2021 is 2.4% higher than the first quarter of the last three years combined ($4.2bn).

Leading this robust turnout in Q1 2021 has been strong deal activity in the consumer discretionary and healthcare sectors. The largest transaction of the quarter was private equity giant CVC Capital Partners’ acquisition of Shiseido’s personal-care business, in a deal reportedly worth $1.5bn. Under the terms of the deal, CVC Asia V will acquire a 65% stake in a newly established joint venture that will own the assets, with Shiseido retaining the remaining 35% stake. The move is said to be part of a larger strategic plan to offload non-core assets by the end of 2021.

Yukinori Sugiyama, Partner and Co-Head of CVC Japan, said in a press release about the deal that the firm sees “significant potential for growth by investing further in employees, brands, and R&D, as well as by driving digitalization and accelerating overseas expansion, with the possibility of going public in the future.” Importantly, the comment points to no shortage of value levers at the disposal of CVC to pivot the stagnating unit of the more than 140-year-old cosmetic giant toward future growth.

Second in line for the largest transactions in Q1 2021 was the $963mn buyout of precision x-ray and health science analytics instrument manufacturer Rigaku Corporation, led by global firm Carlyle Group. The private equity major announced it would own 80% of Rigaku while the remaining 20% stake will be held by the Chief Executive Officer of the company, Hikaru Shimura. The partnership is said to be pursuing a public listing of the newly formed holding company in the coming years. The deal marks the first investment of the firm’s newest and largest Japan-focused buyout fund, Carlyle Japan Partners IV ($2.5bn), in a buyout market heating up as firms aggressively hunt to unlock succession and expansion opportunities.

“This is an optimal deal for Carlyle in terms of supporting the globalization of a large, owner-managed company. We believe we will see more of these types of deals in the future, which we will proactively pursue, in addition to corporate carve-outs,” commented Takaomi Tomioka, Deputy Head of Carlyle Japan.

The Rise of Foreign GP Participation

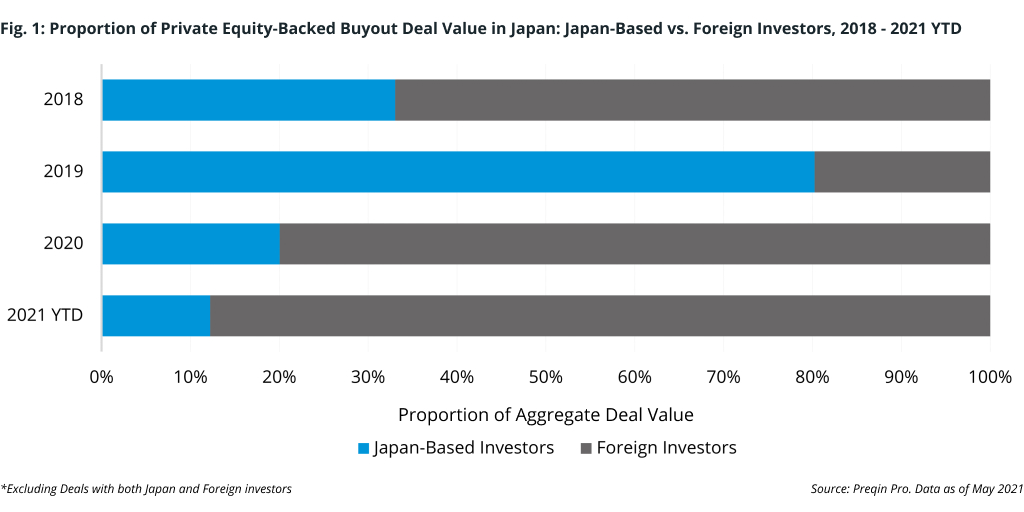

What these two mega buyout deals highlight, besides ample interest in Japanese private equity opportunities, is an ongoing trend of increasing foreign GP participation in deal activity in recent years. Fig. 1 shows a decline in the proportion of deal value led by Japan-based investors since 2018. If we again remove the effects of the DBJ capital reorganization of Kioxia in 2019, the pattern is even clearer, with Japanese investors leading less than half (47%) of deal value in the country that year. More interestingly, perhaps, is that in 2020 foreign investors accounted for a staggering 80% of total private equity deal value in Japan – a record proportion in recent years.

Coming into Q2 2021 this trend shows no signs of stopping. At the end of April, a consortium led by global private equity firm Bain Capital announced it would acquire all outstanding shares of Tokyo-listed Hitachi Metals for JPY 817bn ($7.5bn). The divestment by Hitachi, which owns a 53% stake in the subsidiary, was reported to be part of a decade-long business transition to focus on asset-light digital services from electronics hardware. In addition, the highly anticipated, albeit controversial, $20bn take-private of Japanese conglomerate Toshiba has captivated financial market participants around the world in the past month. The transaction marks CVC Capital Partners and Bain Capital as potential suitors in the running. If completed, the landmark investment would be a major win for shareholder activism and the largest international private equity-led acquisition on record, according to Preqin Pro.

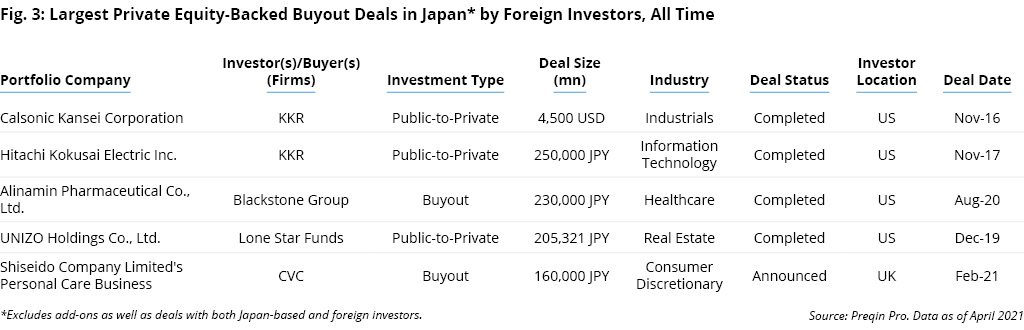

Both deals are far larger than the biggest foreign investor-led transactions recorded in recent years (Fig. 3) suggesting a growing willingness among international mega-buyout funds to bet heavier on the long-term prospects of companies operating in Japan. Fund managers may also be trusting their ability to see through planned value creation strategies and difficult transitions with domestic stakeholders, which have long plagued both public and private markets.

But one thing is for sure, Japan Inc. is bearing witness to a rapidly growing list of notable take-private and carve-out transactions that the alternatives industry will be watching closely. As these private equity firms begin to navigate the nuanced complexities of corporate governance reform in Japan, their success could mark the beginnings of positive change, leading to a more dynamic deal environment and enhanced opportunities for innovation in the coming years.

Pressure Mounts: One Step Forward, Two Steps…

The rising interest among international fund managers is one thing, but local receptivity to growing capital flows is a different story entirely. It is no secret that over the past 10 years domestic management teams and family-owned companies have taken time to warm to the concept of working in concert with any GPs, let alone accept the premise of ‘selling out’ to foreign-owned funds.

In addition, global fund managers have had to contend with expanding public scrutiny of foreign investment in sensitive sectors in recent years. For example, just last year in May the Japanese Government detailed a group of companies comprising half of listed firms that would face new rules restricting foreign ownership in an effort to protect core industries on national security grounds. Although similar to moves by other developed nations during the pandemic, critics were quick to point out the policy could limit long-awaited traction in activist investing and foreign influence in Japan’s capital markets.

While it is easy to write off the progress being made in Japan’s private equity market to a long-term ‘waiting game,’ it is important to note domestic pressure for growth and competitive transformation is at an all-time high. Activist shareholders have increasingly tried to flex their muscles at the bargaining table following reforms to the Corporate Governance Code by the Japan Exchange Group in 2018. In August 2020, Warren Buffet placed a $6bn wager on five of the preeminent sogo shosha (major Japanese trading companies) which was widely held as a vote of confidence by the Oracle of Omaha in the development of a more shareholder-friendly environment. Indeed, the bigger bids by global private equity fund managers this year could finally mean a larger voice for international shareholders, as the drive for value mounts.

For the public sector, charting a path out of the pandemic will face unique challenges. Japanese Government gross debt has marched unabated to a record 257% of GDP this year, according to IMF data. This debt load looks set to continue ballooning in the short term. In March 2021, Japan’s parliament passed a record budget worth almost $1tn for the next fiscal year, which follows three COVID-19 packages valued at a combined $3tn already rolled out. Amid the significant structural issues facing the economy, recovery plans to reach sustainable debt and growth levels will need to carefully consider the capital resources and expertise available from both domestic and foreign sources.

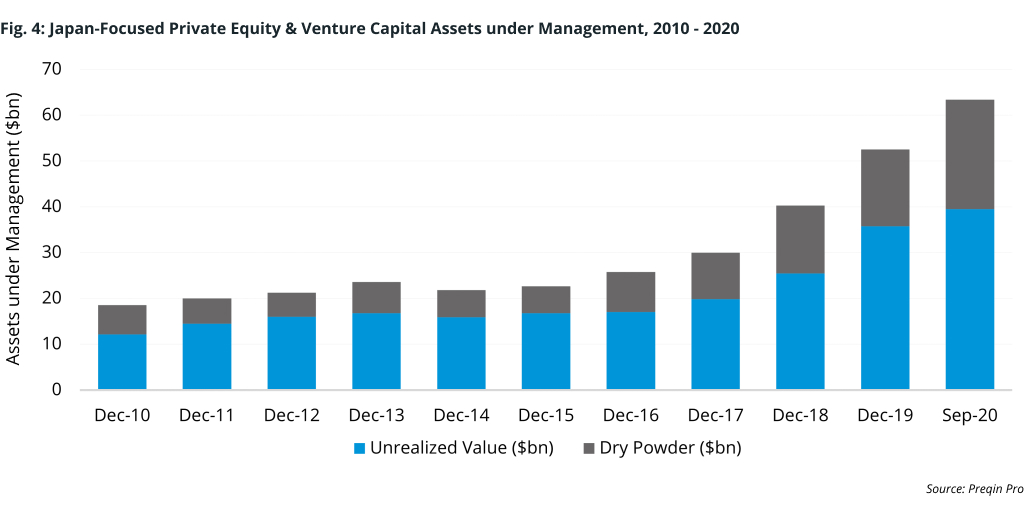

The prospect of a more dynamic private equity market in the coming years looks favorable. When it comes to putting your money where your mouth is, private equity firms are well positioned. Asia-Pacific-focused (including Japan) private equity & venture capital industry assets under management (AUM) stand at a record $1.3tn as of September 2020. Looking specifically at Japan-focused funds, AUM hit an all-time high of $63bn – up 19% on December 2019 figures – comprised of $24bn in dry powder earmarked for opportunities available in the country (Fig. 4). For all fund managers vying to take part in this increasingly vibrant private equity market, this will likely mean fending off rising levels of competition.

While global GPs dominate the deal rosters for the largest buyout transactions in Japan, local managers may find a competitive advantage tapping into transactions in the lower middle market where localized relationship building is more important and deal flow is still largely unencumbered by foreign GP participation. Moreover, this segment of domestic SMEs will increasingly need to look for new avenues of growth, including the internationalization of their operations, which could mean business owners will be more receptive to private equity injections going forward. For Japan, local SMEs are the backbone of commerce supply chains that make up the formidable keiretsu production networks. As the country’s conglomerates face rising pressure to adapt to competition on the world stage, so too will these supporting entities have to embrace change.

In any case, regardless of the segment targeted by fund managers, the investment prospects for private equity in Japan are getting stronger. 2021 could mark the start of a new beginning for dealmakers willing to commit and lend their expertise to guide companies through the transition.