Since the Global Financial Crisis, private equity has shown it can provide investors with strong performance and less volatility – but today’s market conditions present a fresh challenge

Since the Global Financial Crisis, private equity has shown it can provide investors with strong performance and less volatility – but today’s market conditions present a fresh challenge

Private equity’s (PE) strong performance and low volatility have helped the industry to secure huge sums of institutional capital. Over the past decade and more, the industry has shown it can insulate portfolios from public equity downturns. Privately held businesses aren’t required to report their performance publicly each quarter, shielding them from the large swings in valuation that listed companies face. And portfolio companies aren’t as exposed to headline risk the way public companies are. What’s more, longer holding periods mean GPs can wait until the time is right to value and sell an asset.

The combined effect smooths returns. That helps LPs counterbalance the impact on their portfolios from public-equity volatility. But can LPs continue to expect PE to deliver high returns and low volatility under today’s market conditions? Before answering that question, let’s look at PE’s track record. Between 2008 and 2009, during the Global Financial Crisis, the S&P 500 registered a maximum drawdown of 40.4%. By contrast, the PrEQin Private Equity Index fell by just 26.6% (Fig. 1). Similarly, during the 2011 US Debt Ceiling Crisis, the S&P 500 posted drawdowns in 2015, 2016, and 2018, but the PrEQin index barely declined. More recently, in the wake of COVID-19, the PE index dropped in step with public markets, but has since recovered.

But the PE industry has never had to grapple with the confluence of market conditions we are now experiencing. Inflationary pressures are intensifying. Globally, prices are rising at rates not seen since the early 1980s. Interest rate hikes have had little impact since a root cause underlying rising prices is supply-side issues. At an analyst briefing this month, JPMorgan Chase & Co CEO Jamie Dimon warned of an ‘economic hurricane’ brewing, spurred by inflation, quantitative tightening from the Fed, and the war in Ukraine.

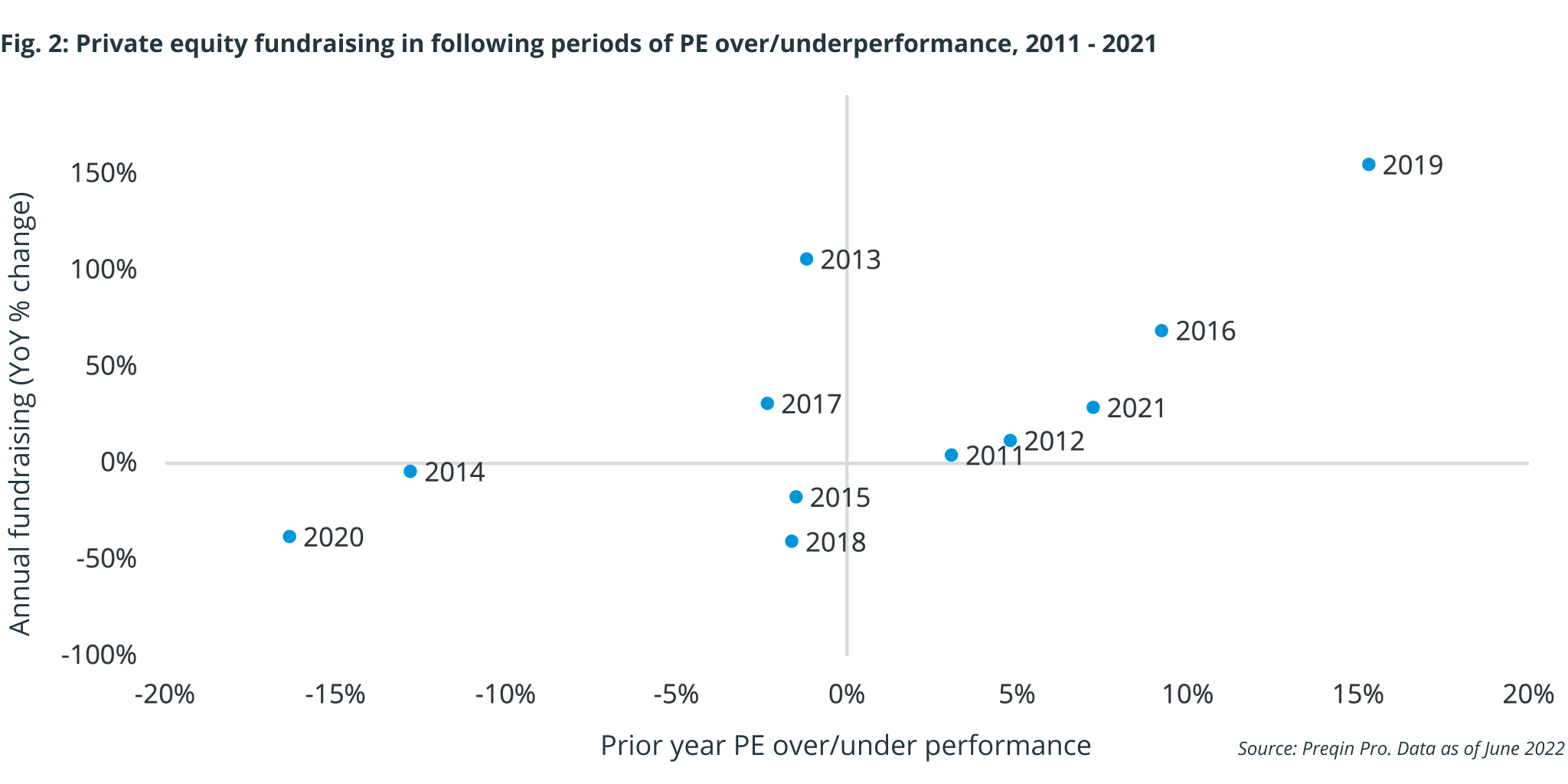

The attractions of smoothed returns

PE’s smoothed returns have been a key attraction for investors. This is portfolio efficiency at its best. Preqin fundraising data shows a steady upward trend of cash flowing into the industry, regardless of market conditions (Fig. 2). Indeed, in recent periods of stress or public equity underperformance, investors allocated even more to private markets, particularly PE, contrary to a concept called the denominator effect.

Re-up or reallocate

In short, the denominator effect forces allocators to rebalance toward public equities following a downturn, as fallen valuations result in a portfolio that’s underweight in the asset class. In this case, with both US equities and global equities down 14% over the first five months of 2022, and US investment-grade debt down 8.3% through May – a rarity for the 60/40 portfolio – private capital markets should expect some downward pressure on fundraising. But given recent fundraising and allocation trends, this scenario is unlikely thanks to private equity’s outperformance and low volatility. As shown in Fig. 2, fundraising in 2021 bounced back sharply from a low in 2020 due to outperformance. So even amid a down public equity market, allocators are likely to favor private markets. But what will those markets look like?

In a recent op-ed in the Financial Times, industry veteran Mohamed El-Erian pointed specifically to higher interest rates as a frequently overlooked area of risk. He noted that higher rates will complicate the financing and refinancing of transactions, and also touched on the impact a recession would have on portfolio companies’ bottom lines. The US Federal Open Markets Committee has raised its base interest rate three times so far year, setting the upper bound of its base overnight rate at 1.75% following its June 15, 2022 meeting.

Private equity has proven its resilience in rough markets and managers are unlikely to stop deploying capital just because market parameters have changed. This resilience has driven a flood of institutional cash into the industry, with the expectation of generating similar results. However, recent vintages’ performance may still disappoint. Deal multiples have been on the rise over the past five years, but are slowing as rates have ticked higher, particularly in the tech sector. The high entry prices of 2020 and 2021 may prove trickier for finding value on the way out for allocators who bought at the peak.