Private capital is mobilizing to plug Asia’s green infrastructure funding gap, but the region’s emerging markets remain underfunded

Private capital is mobilizing to plug Asia’s green infrastructure funding gap, but the region’s emerging markets remain underfunded

The green transition in Asia is well under way. Governments from Singapore to Hong Kong have renewed their climate pledges over the past year, laying out ambitious new plans for sustainable infrastructure. In September 2020, China surprised the UN with its goal to achieve carbon neutrality before 2060. And in Indonesia, the government is seeking investors to seed a $20bn sovereign wealth fund to revive its economy from a pandemic-induced recession and accelerate infrastructure development.

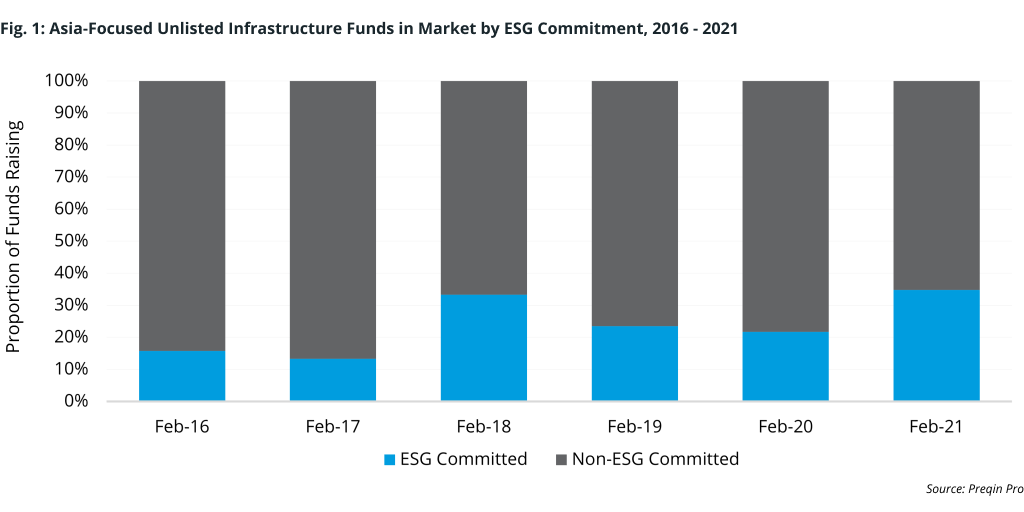

Private capital is expected to play a big role in plugging Asia’s green infrastructure funding gap, and funds are already being mobilized. Preqin data shows there are currently eight Asia-focused infrastructure funds on the road managed by firms with environmental, social, and governance (ESG) policies, up from just five at the end of February last year (Fig. 1).

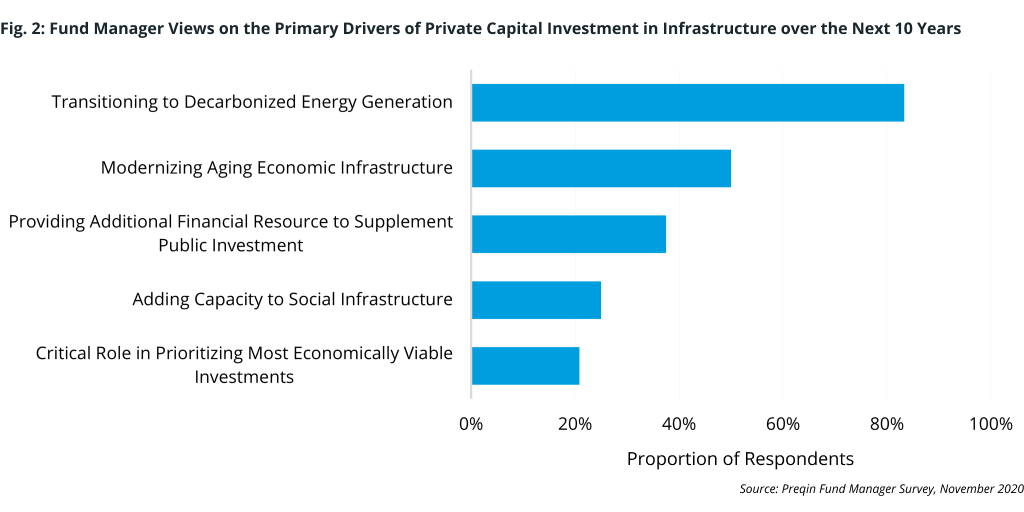

Indeed, 83% of global infrastructure fund managers polled by Preqin toward the end of 2020 said they believe that the transition to a decarbonized energy generation system will be a key driver of opportunity over the next 10 years (Fig. 2), with modernizing aging economic infrastructure ranked second (50%).

But, with the green transition in Asia, something of a dichotomy exists between developed and emerging markets.

More Investment Needed in Emerging Asia

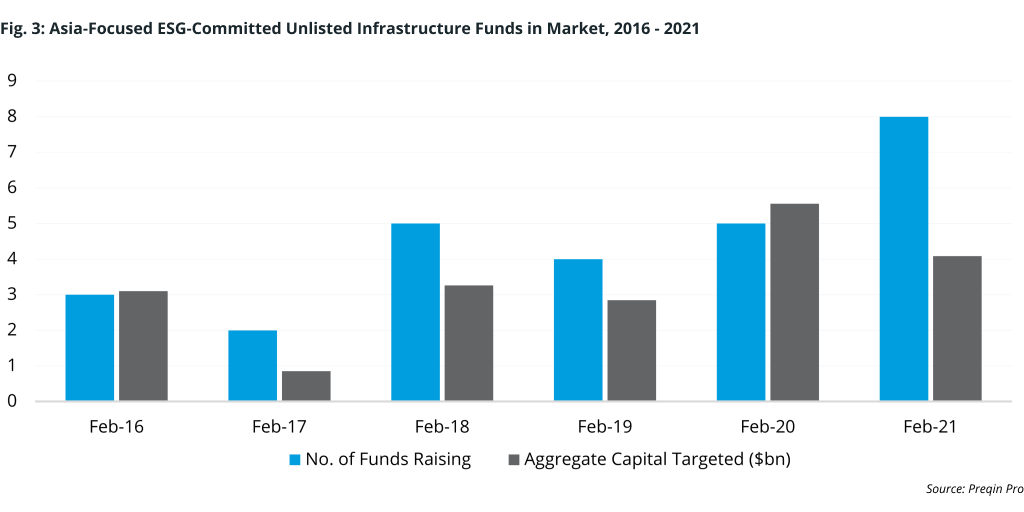

While recent investment trends have been promising, the actual volume of investment is still well below target, according to the Asian Infrastructure Investment Bank (AIIB).¹ OECD surveys observed that pension fund allocations in unlisted infrastructure assets, much less sustainable unlisted infrastructure, were flat over 2013-2017. As Fig. 3 shows, capital targeted by Asia-focused, ESG-committed infrastructure funds on the road amounts to only $4.1bn, down from $5.6bn targeted by fewer funds at the same time last year.

For emerging markets in particular, the picture is more troublesome. Despite the opportunities to invest in much-needed infrastructure development, many barriers still exist for private capital players. The OECD surveys point out that institutional investors have generally avoided large commitments to greenfield infrastructure in emerging markets. The AIIB observed: “Several major obstacles [inhibit] increasing emerging markets infrastructure investment by institutional investors, namely a significant J-curve for cash flows from greenfield assets, excessive perception of EM risks, and large efforts required to make projects ‘bankable’.”

The Developed and Emerging Market Divide

This contrast between the perceived risks facing infrastructure investments in developed Asia vs. emerging Asia will likely persist – and could dictate regional private capital flows from investors for some time to come. The ramifications of this for sustainable infrastructure development, the energy transition, and climate change could be significant.

On the one hand, advanced Asian economies present attractive opportunities to invest in the energy transition, according to Stephen Panizza, Head of Renewable Energy at Federation Asset Management, which invests across Asia-Pacific but primarily targets opportunities in Australia. “Japan, Korea, and Taiwan are large and attractive markets, with offshore wind offering great potential,” he says.

However, Panizza also notes that institutional investors are not investing as much in greenfield infrastructure in Asia’s emerging markets. “Emerging markets offer promise as high-growth markets; however, renewables investment in these markets is also more challenging,” he adds.

“Investors must grapple with long-dated assets that have to be built and operated in under-developed legal and regulatory environments, in illiquid local currency capital markets, and with higher sovereign risk. Energy generation projects are in demand, but in markets without feed-in tariffs or other government support mechanisms, the offtake (power purchase agreements) can be an impediment to growth in renewables. Projects with material exposure to merchant energy prices are challenging to finance,” says Panizza.

Priscilla Lu, Head of APAC Sustainable Investments at DWS, agrees: “Green infrastructure, like all infrastructure projects, are subject to local country regulatory policies as well as availability of local bank-level financing. Availability of the latter is critical to ensure viability of the projects. Private capital can come in as equity to support developers in the build-out stage of the infrastructures, while long-term bank loans would provide the financing of the projects after launching the operations upon completion of the projects. This complementary play between private capital and bank loans is critical to making projects successful.”

She adds: “Any emerging market infrastructure investment would be subject to some forex risks, and you also need to have a local team on the ground to provide the know-how and expertise to navigate regulatory compliance. Both would need to be taken into consideration in the assessment of the opportunities for any emerging market infrastructure investments.”

For Lu, China – which represents more than a third of the world’s renewable energy production capabilities – is the place to be. “The Chinese Government has supported renewable energy investments by providing readily available loans for developers, thus offering investors additional leverage on their investment capital,” she notes.

“Given the continued focus and priority of the government to keep up the momentum of the build-out, as presented in the draft of the 14th Five Year Plan, we can see renewable energy capacity doubling over the next 10 years. This represents a tremendous opportunity for private capital to invest and get steady, acceptable returns on their investments,” Lu adds.

The Path to Greener Outcomes

If international climate goals are to be met, more needs to be done to catalyze renewables investment in Asia’s emerging markets. As policymakers in these regions mull over strategies to lift their economies out of the COVID-19 slump, fiscal rather than monetary stimulus may be the better way forward. Better still if this stimulus takes the form of green infrastructure programs and the roll-out of green financing options to spur private investment in the sector. A closely integrated approach between private capital and government could significantly improve progress toward sustainable development in the region.