Backed by government efforts to enhance shareholder value, activist hedge funds in Japan are becoming increasingly aggressive in their demands

Backed by government efforts to enhance shareholder value, activist hedge funds in Japan are becoming increasingly aggressive in their demands

Investor activism is attracting more attention in Japan, with Dai Nippon Printing (DNP) and Seven & i Holdings recently succumbing to pressure from investors. In response to investor campaigns, DNP launched its largest share buyback program in February, while Seven & i Holdings, the parent company of 7-Eleven, announced its latest restructure the following month.

The share prices of both companies gained on the day of their respective announcements, as markets took them as a sign that Japanese companies are becoming more responsive to the drive by the government and activists to improve shareholder returns. DNP’s shares soared by a record 18% after the firm unveiled its share buyback plan, just weeks after US activist fund Elliott Management bought a substantial stake in the company.

Seven & i’s shares also rose by 4.1% on March 9 ─ the largest gain in two months ─ after it announced the closure of one in every four of its Ito-Yokado stores in Japan, as well as the full exit of its apparel business. It has been under pressure from US activist hedge fund ValueAct Capital, which has a 4.4% stake in the company, to focus on its lucrative 7-Eleven business, which generates 97% of the group's profit.

However, Seven & i’s shares fell by 5.4% on March 10 after a rating cut by brokerage CLSA Securities Japan, as its new business plan lacked any mention of spinoffs. The continued weakness in Seven & i’s shares prompted ValueAct to lobby for the ousting of four directors over ‘governance failures’ just weeks later. This is seen as ValueAct’s most assertive move away from its usual management-friendly approach, which it once said sets it apart from other ‘transactional’ activist funds.

According to ValueAct, spinning off retail businesses that have very limited synergies would more than double the share price and boost the long-term corporate value of Seven & i. However, it’s clearly been frustrated at the rate of progress, abandoning its non-confrontational policy for the first time last year in a public letter to Seven & i's Board of Directors.

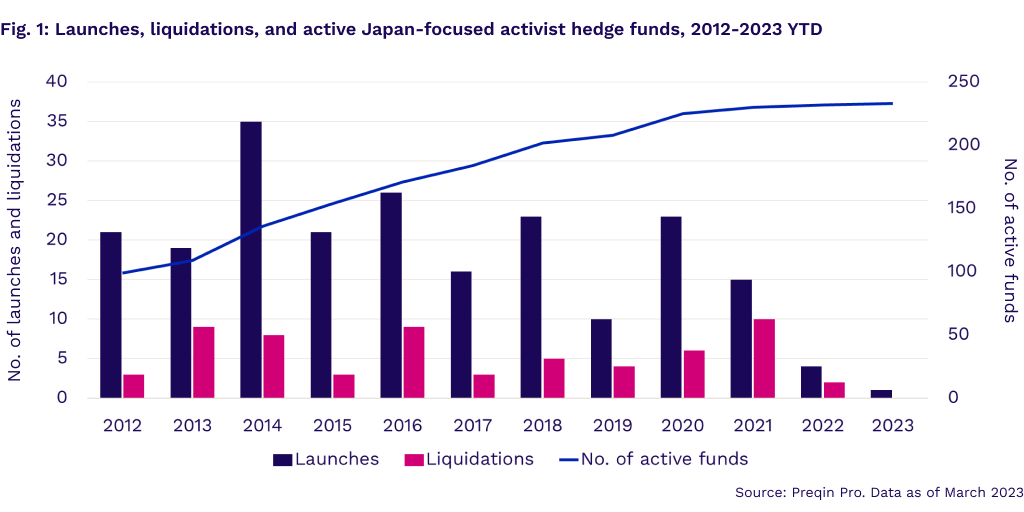

Japan-focused activist hedge funds at record high

The number of active Japan-focused activist hedge funds have been on a steady rise, more than doubling from a decade ago (Fig. 1). There are currently 233 activist hedge funds in the market.

In particular, ValueAct has been the most active recent player and the only activist fund with substantial capital deployed in Japan. Around a quarter of its $16bn assets under management are invested in Japanese companies, and it’s launched three out of the five Japan-focused activist hedge funds since 2022. The $13bn San Francisco-based activist investor launched its first two Japan-focused activist hedge funds in 2019. These launches build on its first successful friendly Japanese investment in Olympus in 2017.

Despite the focus on activism in Japan, a closer examination reveals that activist hedge fund activity has been slowing over the past few years. Only four such funds were launched last year and just two have been liquidated, suggesting a sluggish year for activist hedge funds. The cooling sentiment in 2022 contrasted with the previous year, when activist hedge funds hit a record high of 10 liquidations and a relatively robust 15 fund launches.

The modest stake of most activist hedge funds means that they require major shareholders to support their strategy. However, many of the companies in question are backed by large domestic players that are still sceptical of opportunistic action by foreign funds. For instance, the major corporate shareholders of DNP include Dai-Ichi Life Insurance (3.4%), Mizuho Bank (2.1%), and Nippon Life Insurance (1.8%), all of which support corporate cross-shareholdings.

Cross-shareholdings can contribute to prolonged underperformance, as such alliances encourage management to focus on business relationships instead of profitability. Many Japanese companies maintain these shareholdings as a defence against hostile takeovers. This has made efforts to solicit change an uphill task, and creates a difficult situation for many activist funds. Nevertheless, the Japanese government has been trying to reduce such cross-shareholding as part of its long-term goal to improve corporate governance.

Toshiba serves as a classic example of a proxy fight in Japan, where activists have engaged in a prolonged battle with the company. Their efforts have included launching campaigns to demand board changes, voting against management's plans, and advocating for the company's privatization. Although overseas-based players like Bain Capital and CVC have submitted bids, Toshiba ultimately accepted a JPY 2tn bid on March 23 from domestic private equity firm Japan Industrial Partners (JIP) for a take-private deal, in what would be the largest deal of its kind in the country's history. The conglomerate backed JIP as the preferred bidder to maintain domestic influence. While it's unclear if activists are content with the buyout price, JIP's proposal is the only complete offer Toshiba received during the one-year auction process, and provides an exit opportunity for activists.

Japan on verge of deep reforms

The Japanese government has been adamant about improving shareholder returns by introducing a revised Corporate Governance Code. The initiative is intended to address the chronic underperformance of Japanese stocks. About half of Japanese companies are trading below their book value, plagued by issues around corporate governance and capital management.

As a result, market reforms have been introduced across Japan that aim to address these long-standing structural issues and boost investor confidence in the ability of companies to generate returns. For example, Tokyo Stock Exchange has urged companies trading below book value to address their underperformance from this spring. This is a sign of the increasing pressure companies are under to improve valuations and shareholder returns – a tailwind for activist investors in Japan.