As the pandemic increases the need for social infrastructure and the importance of defensive allocation options, investor interest in impact real estate investment could rise

As the pandemic increases the need for social infrastructure and the importance of defensive allocation options, investor interest in impact real estate investment could rise

In recent years, private real estate fund managers have increasingly adapted their frameworks to consider environmental, social, and governance (ESG) criteria in response to LP demand. The number of new fund manager signatories to ESG/impact investing frameworks increased every year between 2014 and 2018, reaching a record high of 37 in 2018, as the chart above shows. Despite a fall in new signatories the following year, adoption is still widespread with 427 signatories in total as of November 2019.

COVID-19 could accelerate this trend. The current pandemic has highlighted the shortcomings of public healthcare systems in vulnerable communities around the world. New challenges are mounting on existing social and economic inequities, raising awareness of the need for investment capital to bridge the gap for more sustainable and equitable development. And impact investors are seizing the opportunity. Despite current economic headwinds, a majority (67%) of impact investors expect to maintain or boost their commitments to impact investments this year, according to a survey by the Global Impact Investing Network (GIIN).

Looking more specifically at the private capital industry, momentum is also growing. A Preqin survey of alternatives investors at the start of 2020 showed almost two-thirds (61%) expect ESG to become more integral to the industry in the next 36 months. And with close to $8tn in assets managed by private capital firms as of September 2019, private capital could play a leading role in delivering impact in the wake of COVID-19.

The Evolution of ESG Investing in Real Estate

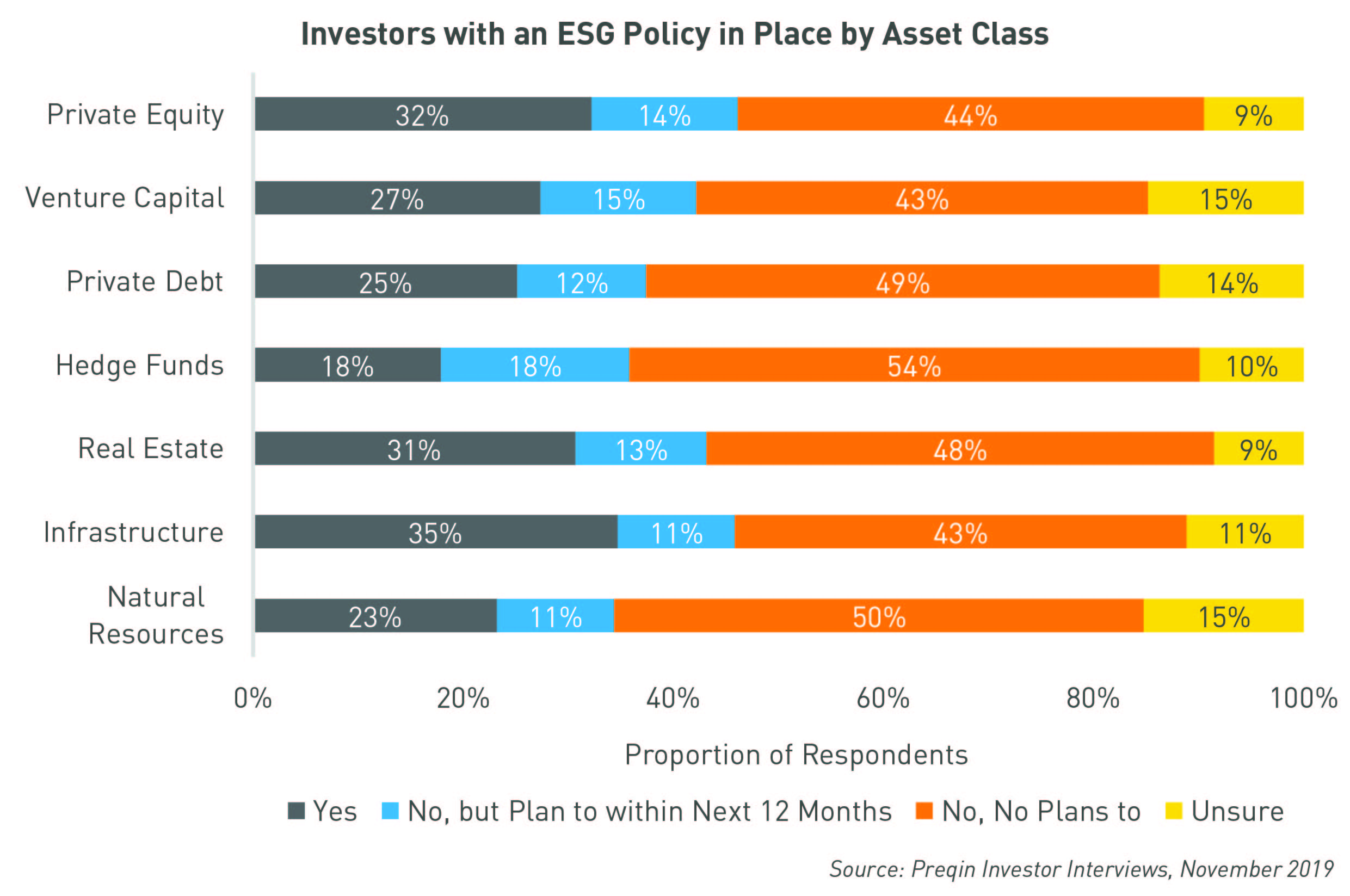

As a single asset class, private real estate has emerged as a prominent fixture of the impact investing landscape. Given its direct ability to revitalize urban areas, provide access to affordable housing, adopt environmentally friendly practices, and ultimately build more resilient communities, it is no wonder that real estate LPs are now among the most active adopters of ESG policies across alternatives. The chart below shows 31% of real estate investors surveyed by Preqin in November 2019 had an ESG policy in place, close behind infrastructure (35%) and private equity (32%), as reported in the 2020 Preqin Global Real Estate Report. Furthermore, an additional 13% of private real estate investors planned to implement ESG policies in the next 12 months, bringing the expected total to 44% by 2021.

This move by investors toward the greater adoption of ESG and impact policies is “simply smart investing,” explained Bobby Turner, CEO of California-headquartered Turner Impact Capital. “While most real estate investors are speculating on creating demand that may or may not exist for things like hotels or high-end condos, investing to address daunting social issues like education, affordable housing, and healthcare is serving significant demand that is going unmet.”

Governments are the traditional investors in social infrastructure, but keeping up with a growing need for public services is proving difficult. Despite increasing pressure to step up the rates of public infrastructure development, government investment as a share of GDP globally has been falling since the 2008 financial crisis – widening the gap between accelerating needs and shrinking budgets, according to Deloitte. This has pushed the public sector to embrace new models of financing involving private sector participation in the public delivery of services.

“Reliance on government spending alone to address significant social issues has come up short,” said Turner. “A great example is affordable housing. Half of families in America spend in excess of a third of their income on rent. While a quarter, more than 12 million families, are severely rent-burdened – spending 60% of income on rent – at the expense of food, health, and retirement security.”

The impact of COVID-19 is going to make things more difficult. “This crisis is hitting these vulnerable and disadvantaged populations the hardest. It is also going to further exacerbate the government’s inability to create lasting solutions to some of our most pressing challenges,” Turner highlighted.

Indeed, COVID-19 is already testing the fiscal limits of various levels of government around the world, which are struggling to fund critical social safety nets. As these pressures mount, additional sources of financing will be required to fund shortfalls for community-serving infrastructure – a gap private real estate is well positioned to fill.

The current crisis is challenging real estate investors to re-examine their asset allocations, as well as the role ESG investments can play in building more resilient communities and portfolios.

How COVID-19 Has Impacted Real Estate Investors

“At the start of 2020 the outlook for private real estate investment was in a strong position and well capitalized,” said Troy Merkel, Partner, Real Estate Senior Analyst at global audit, tax, and consultancy firm RSM. “It was clear that investors were still attracted to real estate, but there were challenges following a prolonged expansion period and a low interest rate environment. Cap values across most assets were driven to record lows. As such core and core-plus investments were flat, so funds were targeting debt and value add opportunities in pursuit of yield.”

Dirk Aulabaugh, Managing Director, Global Head of Advisory Services at California-headquartered Green Street Advisors, added that “the real estate market did indeed exhibit decent fundamentals, but there was a greater bifurcation between sectors. Retail rents for example were barely holding up, while you had decent fundamentals in certain residential assets.”

Similarly, the impact of the COVID-19 crisis from a sector perspective has also been uneven. “What I would call ‘beds and sheds’ have been strong and resilient. Sectors like single- and multi-family rental housing, as well as niche industrial assets like logistics, have done well,” said Aulabaugh. “But, most traditional real estate sectors like lodging, malls, and offices have been hit hard. In fact, malls for example have collected less than 30% of their rents during lockdowns in most cases.”

Merkel added that, with so much uncertainty surrounding the economy and the way we will use real estate in the future, investors are taking a ‘wait-and-see’ approach, especially with regards to hotels, retail, and office investments. Multi- and single-family rentals, and industrial assets – on the other hand – are still attracting investors, but with slower activity.

With many traditional commercial real estate assets hit hard by the crisis, investors have picked up the hunt for assets that might be better positioned to weather a downturn. “Since COVID-19 hit there has been an acceleration of investors moving into these more resilient sectors; not a wholesale change in strategy, but clearly an additional focus on defensive niche sectors relative to traditional areas like office buildings or retail,” Aulabaugh explained.

Impact Real Estate as a Defensive Play

With LPs looking for more resilient real estate opportunities, impact investing could be an untapped opportunity set with an increasing need for capital.

“The crisis is confirming that the demand for community-serving infrastructure is huge and growing. It is also proving impact investments like ours are less correlated to broader market indices and economic conditions compared to most other real estate investments. If done correctly, investing in densely populated, ethnically diverse communities will drive alpha and defensive diversification for your portfolio,” Turner said.

“The demand for things like affordable housing, preventative healthcare, and great education is not going anywhere – if anything it’s growing right now. The same can’t be said for hospitality or high-end condos where demand is being eviscerated.”

Despite the merits of impact investing for real estate, it is still misunderstood by investors. “Most underserved communities have been neglected by investors primarily because there is a perception that there are additional risks present that are not identifiable, quantifiable, or mitigatable,” Turner explained. “Investors tend to look at poor communities as lacking the essential risk/reward ratios that you are looking for as an investor.”

Indeed, performance still matters for investors, but doing good does not have to come at the expense of attractive risk-adjusted returns. “As an impact investor I can drive competitive non-correlated returns while at the same time improve the opportunities for a vast number of families. Our school funds deliver north of 8% return net of all fees, and our affordable workforce housing funds deliver 10%, like our healthcare fund,” noted Turner. “You will underperform a bull market because identifying, quantifying, and mitigating risk may come with reduced return. On the other hand, I will always outperform a bear market because my underlying demand is just not correlated.”

Outperformance boils down to selecting the right fund manager. This is especially true during times of uncertainty and crisis.

What to Look for in a Real Estate Fund Manager during Uncertainty

“First, investors need to look for a long-term track record through market cycles,” said Aulabaugh. “When you are in an environment like today, you want to back fund managers who have been here before and have focus on their real expertise. They need to be able to articulate a clear vision that you can really believe in.”

In addition to having a track record through times of crisis, investors should be on the lookout for fund managers with “a conservatively leveraged portfolio,” said Merkel. “It is usually these grizzled veterans that have kept leverage low over the past 10 years and are in a position to absorb cash flow shortfalls without threatening to default on their lending facilities.”

Turner identified three traits of firms that consistently outperform their peers. First, successful funds “lead proactively” with a plan to overcome anticipated challenges, especially so in times of crisis – “hope is not a strategy.” For example, Turner Impact made sure to tap funding relationships early when COVID-19 first hit, to make sure the firm was ready should a need arise. It also quickly assembled a crisis response team to better educate and help its tenants during the pandemic.

Second, successful funds are transparent and communicate frequently with all stakeholders from investors to tenants. Lastly, they need to have what he calls a high “adaptability quotient (AQ),” not just IQ. AQ measures the capability of a fund manager to adapt to uncertain situations. Funds that thrive can get comfortable with being uncomfortable quickly. This can partially come from building a diverse and resilient team that brings together a variety of different skills, perspectives, backgrounds, and capabilities – rather than your typical collection of MBAs and JDs.

These fund manager traits are not easy to come by on their own, but impact investing adds a further complication to manager selection. Turner highlighted it is important to recognize that impact investing requires a very unique set of skills and perspective, as well as an understanding of the communities you invest in, which is not easy to replicate.

The Future of ESG in Real Estate

ESG adoption in the private real estate industry has been growing in recent years. And now, as a result of COVID-19, there is increased awareness of the need for impact-oriented capital to address pressing social issues. As investors re-examine their portfolios through this lens and assess the defensive role it can play, we could see an acceleration in ESG policy adoption by GPs and LPs.

“ESG has definitely become more of a topic of discussion,” said Aulabaugh. “The market was moving in that direction already, but COVID-19 is accelerating this trend. With a renewed focus on health, air quality, and building systems, even things like LEED certification will become more important for tenants and fund managers going forward,” he added.

The time is now, to put theory into practice and make a difference. “The current crisis will enhance the focus on socially responsible investing, as it has renewed a sense of community throughout the public psyche,” Merkel said.

“We have got to figure out how to address today’s most challenging issues. We need to look forward to anticipate the challenges we will face,” said Turner. “Social impact investing has never been more important than it is today to our society, but it also has never been more rewarding as an investor.”

For more insights and analysis on the impact of the pandemic on alternative assets, take a look at our COVID-19 Knowledge Hub.