The trend of retail investors seeking alternative sources of returns that can offer diversification from traditional markets will be a significant force for change over the next five years

The trend of retail investors seeking alternative sources of returns that can offer diversification from traditional markets will be a significant force for change over the next five years

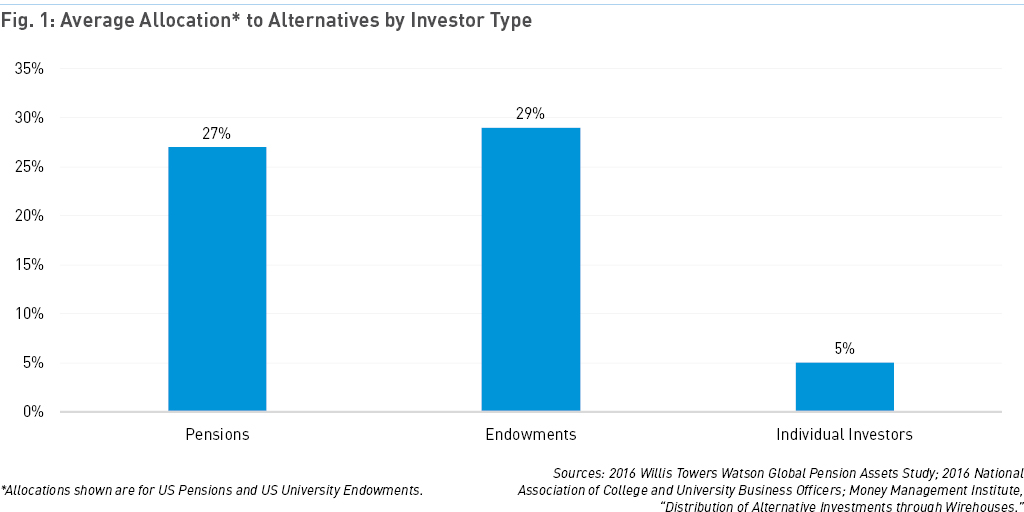

Private market opportunities that have only been accessible to accredited investors at a high minimum investment are increasingly opening up to retail market participation. In August 2020, the US Securities & Exchange Commission expanded its definition of ‘accredited investor’ to allow more investors to participate in private offerings. The SEC expects the total pool of individual investable assets to rise from $70tn in 2018 to $106tn in 2025, while average allocations for individual investors are less than 5%, compared to 27% for pension funds and 29% for endowments (Fig. 1).

Back in June, the US Department of Labor, which governs 401(k) retirement accounts, clarified that under federal law DC pension plan fiduciaries can incorporate certain private equity strategies into diversified investment options, such as target-date funds. Analysts at Evercore estimate that as much as $400bn in new assets, out of the $6.5tn 401(k) market, could make its way into private equity funds.

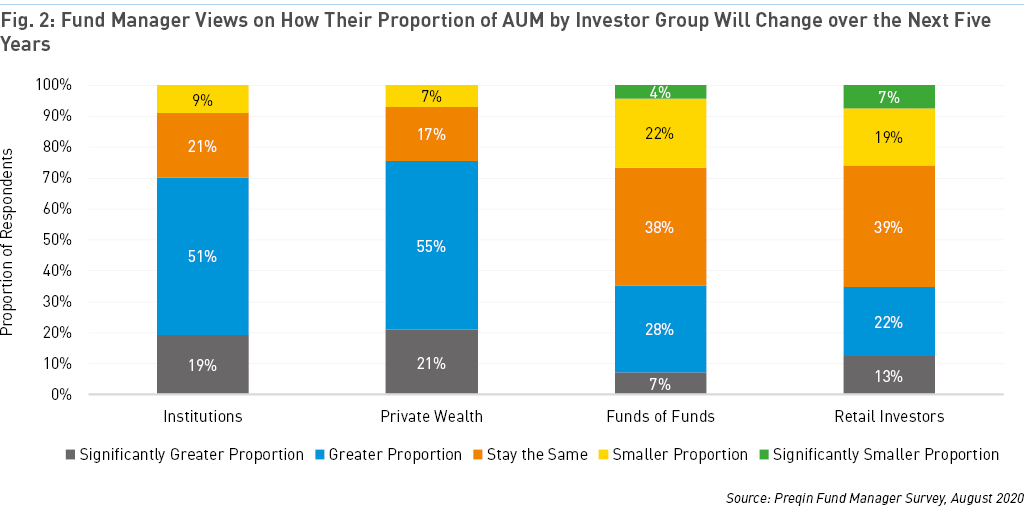

Among alternatives fund managers polled by Preqin for Future of Alternatives 2025, 35% expect retail investors to account for a larger proportion of their AUM over the next five years, compared with 26% that expect the retail proportion of their AUM to decrease (Fig. 2). That flow of retail funds into alternatives over the next five years will likely be slow and steady. To capitalize on any increase in ‘retailization’ in private markets, fund managers will need to add more customer-centric capabilities, such as more frequent and regular reporting, and develop a retail distribution channel.

Liquid Alternatives Grow Rapidly in Europe

Retail participation in hedge funds is more established. Liquid alternative funds – or liquid alts – have become the fastest-growing asset class in the UK- and Europe-domiciled cross-border fund market since the 2008 financial crisis, according to Morningstar’s Cross-Border Liquid Alternative Fund Landscape 2019 study. This is despite what Morningstar admits has been “outright disappointing” results, with liquid alts having generally underperformed hedge funds. Liquid alts are typically structured as mutual funds or exchange-traded funds and employ hedge fund strategies to trade more liquid assets like equities or futures, while providing daily liquidity and valuation.

The sustained popularity of liquid alts in the European cross-border market, as opposed to the US where investor interest has diminished since 2016, has been attributed to lower bond yields in Europe over the past 10 years – a feature that could well characterize the global investment landscape post-COVID-19.

Hedge funds may find it increasingly important to have a retail investor strategy over the next five years. The growth of the liquid alts market is putting pressure on traditional hedge fund fee structures, as mutual fund companies squeezed by low-cost ETFs launch more liquid alternative products. So far, the liquid alts universe has been marked by high turnover and dominated by new, untested strategies with a low asset base.

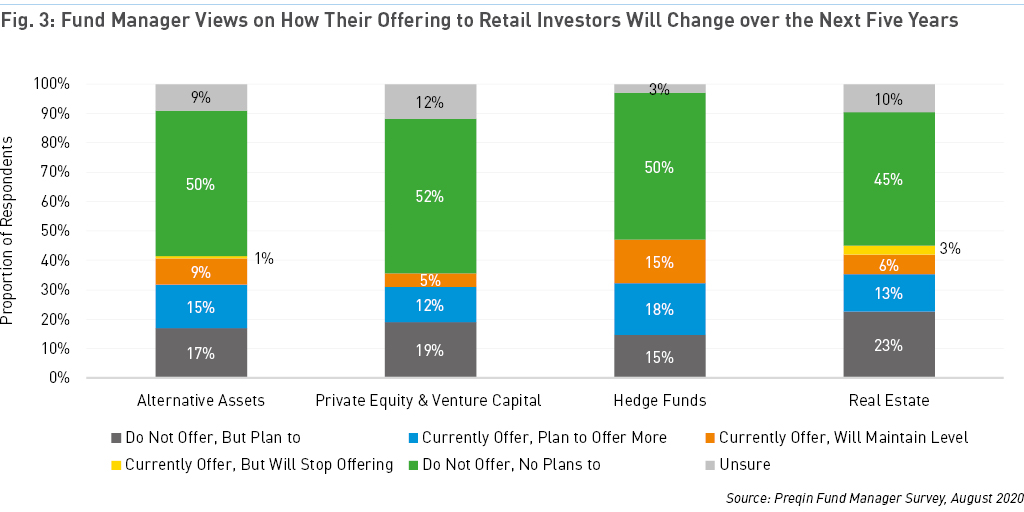

This means that liquid alts could be the next frontier for product innovation over the next five years. Indeed, a poll of alternative asset managers by Preqin shows that hedge funds currently lead in retail product offerings. A third of respondents currently have a hedge fund retail offering, with 15% saying they will maintain their current level of products; a further 18% intend to offer more by 2025 (Fig. 3).

Responsible Investing for Retail Investors

We expect the retail investor contribution to total alternatives AUM to continue to be dwarfed by that of institutions. However, it could have a disproportionately large impact on the profile and reputation of the industry, which could well turn out to be a positive development. In the wider world, the terms ‘private equity’ and ‘hedge funds’ are rarely attached to positive stories. That said, most people who have delved deeper into the workings of these industries have discovered their importance to wider economies and the merits of the model.

Download a data pack containing all the charts in our investor articles for Future of Alternatives 2025. For more predictions and projections from Preqin on the future of the alternatives industry, visit our Future of Alternatives 2025 Content Hub.