Investors’ ongoing search for yield has put private debt in their sights. With further growth expected in Europe and emerging markets, we predict the asset class will be the second fastest-growing alternative, hitting $1.46tn in 2025

Investors’ ongoing search for yield has put private debt in their sights. With further growth expected in Europe and emerging markets, we predict the asset class will be the second fastest-growing alternative, hitting $1.46tn in 2025

Private debt will continue the expansion of the past decade over the next five years. Already one of the fastest-growing alternative asset classes, with total assets under management (AUM) rising 168% from $315bn in 2010 to $845bn in 2019, Preqin expects this growth to continue with a 73% increase in AUM to $1.46tn by 2025 (Fig. 1).

A Bigger Role for Private Debt

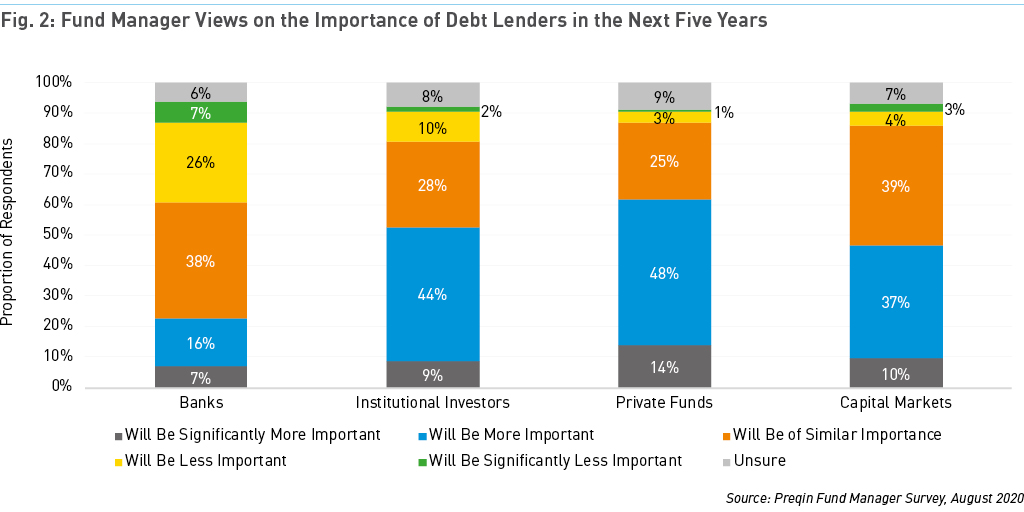

Private debt is sourced from long-term funds and investors that are willing to take on greater risk in anticipation of higher returns. Firms have stepped into a gap left by banks, which have been more heavily regulated since the Global Financial Crisis and are focused on lower-risk credits. A third of all private fund managers surveyed by Preqin for Future of Alternatives 2025 believe banks will be less or significantly less important as debt lenders over the next five years, compared to a quarter that expect them to be more important (Fig. 2).

A substantial majority (62%) of respondents expect private debt funds to play a bigger role over the next five years, with just 4% saying they will be less important. Nearly half (48%) of fund managers also expect capital markets to be a more important source of debt finance. IQEQ says that, with greater appetite for risk than banks, private debt funds will be active in emerging technologies such as pharmaceuticals and the remote working industry.

An Attractive Prospect for Yield-Hungry Investors

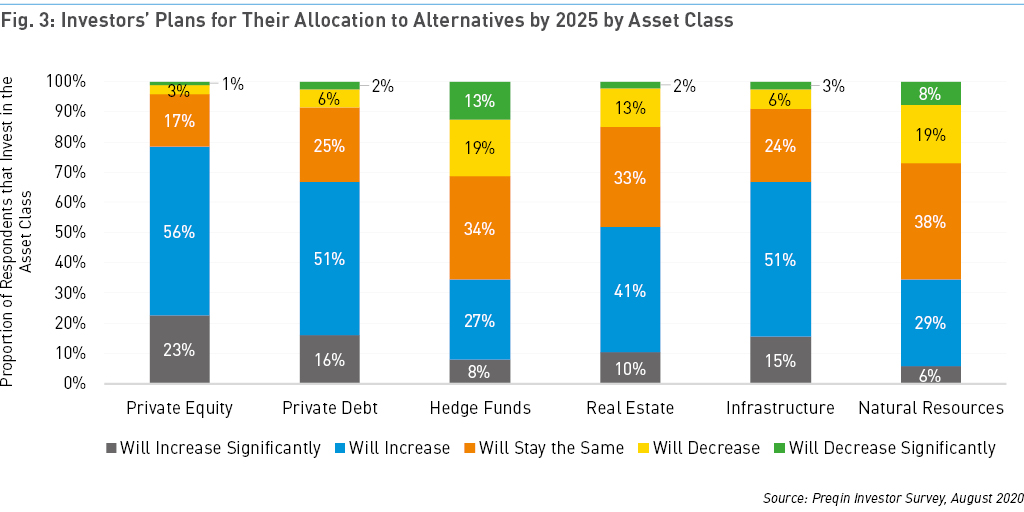

The hunt for yield will continue to drive investors toward the asset class. Of the private debt investors surveyed by Preqin, 58% intend to increase allocations to the asset class by 2025, with only 7% expecting allocations to decrease (Fig. 3). Preqin data shows a horizon IRR of 8.8% over the 10 years to 2019 – and this strong historical performance may be difficult to match. Of surveyed private debt fund managers, 49% expect lending terms to improve over the coming five years, compared with 24% that expect a deterioration.

While direct lending makes up the largest proportion (38%) of total private debt AUM as of December 2019, investors are increasingly turning to distressed situations where they see opportunities now and over the next few years. There are currently a record 79 distressed debt funds in market. Many of America’s largest pension funds, including California State Teachers' Retirement System (CalSTRS) and New York State Common Retirement Fund, have piled into the asset class to capitalize on market misalignments arising from the COVID-19 pandemic.

Emerging Markets Are Coming into Play

While the US has long been the global hub of private debt activity, Europe is catching up. Private debt AUM in Europe has grown by 380% over the past 10 years, and now constitutes just over 20% of total AUM for the asset class. The region will continue to provide more diversification for lenders in the coming years with increasing penetration of the small and mid-sized enterprise (SME) market, while competition is less of an issue than it is in the US.

The Asian private debt market has taken off in recent years. Small and mid-sized companies, which account for two-thirds of jobs in the region, faced an annual funding gap of over $4tn in 2019. Twenty-three percent of surveyed fund managers believe emerging markets currently present the best opportunities, but 39% predict they will offer the best opportunities in five years’ time.

Private debt has by no means been an overnight success. Deal volumes have risen consistently over the past 10 years and the number of funds in market has been increasing each year to meet rising demand, culminating in a fundraising market more crowded than ever before. All the evidence points to continued growth for the asset class, which we expect to overtake the private real estate market in AUM by 2025.

Download a data pack containing all the charts in our asset class forecast articles for Future of Alternatives 2025. For more predictions and projections from Preqin on the future of the alternatives industry, visit our Future of Alternatives 2025 Content Hub.