First-time funds are finding it increasingly hard to find their place

First-time funds are finding it increasingly hard to find their place

Private markets are challenging for first-time fund managers. These managers are new to the asset class or starting out on their own, and their funds continue to see a tougher road to fundraising as LPs move in favor of funds run by more seasoned GPs.

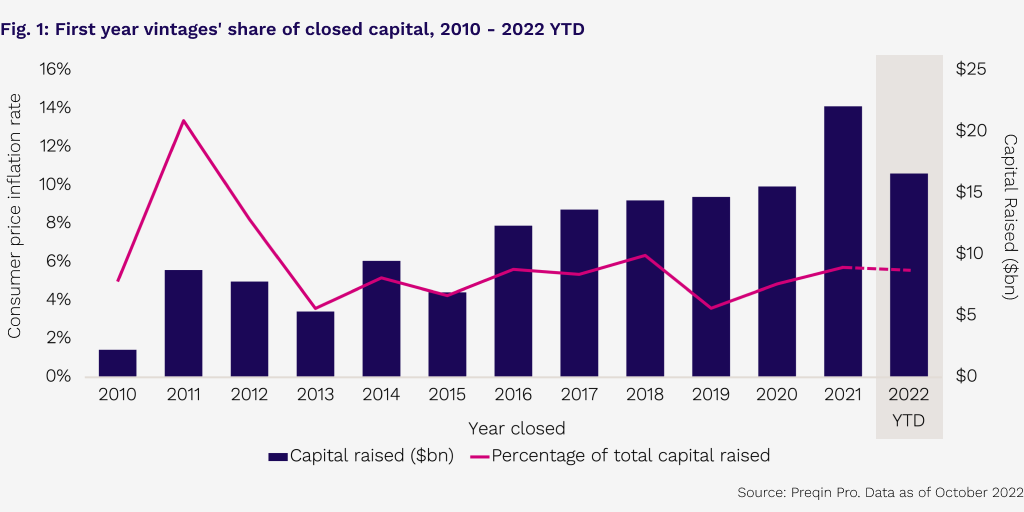

2021 was a record-breaking year for private capital fundraising. Yet that year, first-time funds received less than 6% of the total capital raised (Fig. 1). That share has been steadily declining for much of the past decade as experience and proven performance reign supreme. Of the $885.7bn worth of US-based private capital fund closures last year, $62.4bn was raised by first-time funds. This figure marks its lowest point since 2016.

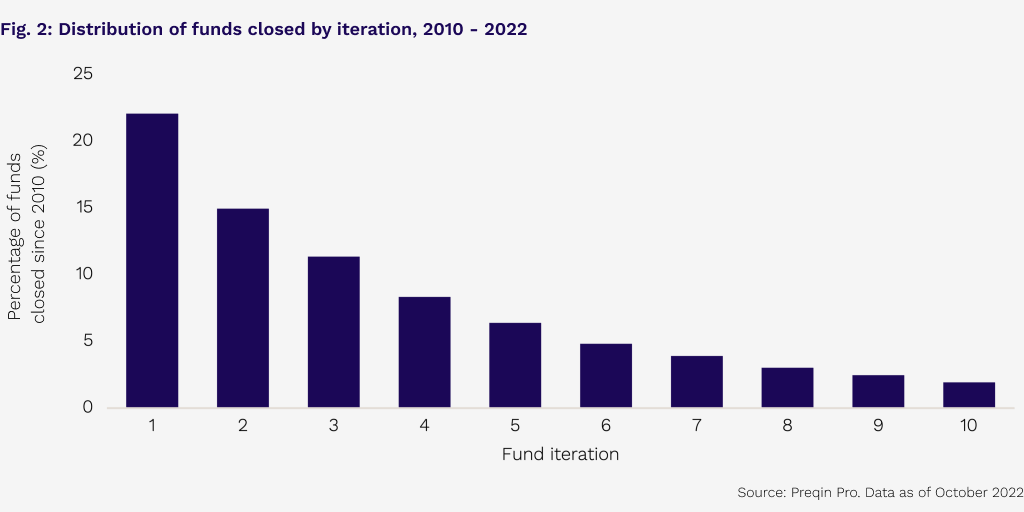

New managers have history working against them. Private capital fundraising is highly dependent on past performance that can pave the way for subsequent fundraising. This is seen most acutely as the number of follow-on funds, or funds that are a second iteration or higher, declines as managers push out the next iterations of their funds. Of the private capital funds closed between 2010 and 2022, 22% were first-time funds (Fig. 2). That proportion drops off significantly as funds progress through the next iterations as success begets success.

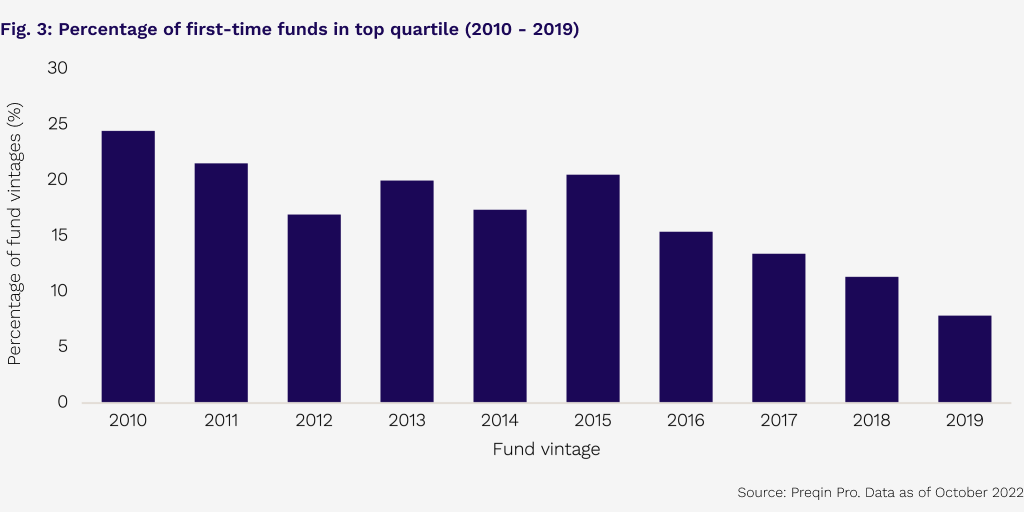

And success for first-time funds is becoming rarer. Since 2015, fewer funds have performed (annualized IRR) above the median universe return. For first-time fund vintages between 2010 and 2015, about 20% of their peers performed above the median of their respective vintage (Fig. 3). More recently, however, fewer than 10% of 2019 vintages have performed above the median as more seasoned fund managers outperformed.

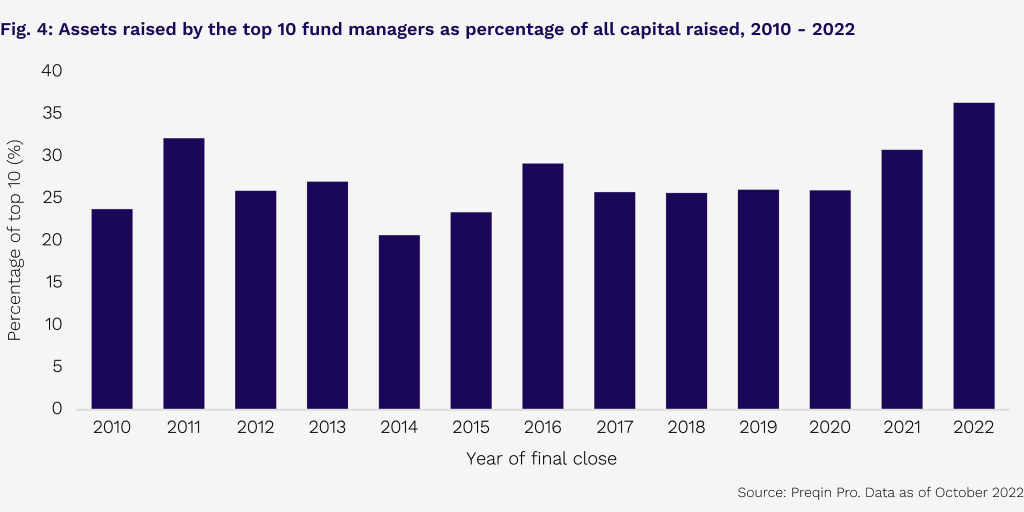

Size and scale are key. Much as private capital managers must pull levers to extract value from their portfolio assets, so too do they require them to operate their broader business as well. More assets means more resources, better leverage terms, and larger networks. These conditions mean that an average of 25% of annual fundraising has gone to just the top 10 managers over the past decade. A number that spikes in years of high volatility, such as 2011, 2016, and 2022 (Fig. 4).

What’s more, relationships matter, and smaller LPs, or those new to private markets can get excluded from the seasoned top performers in favor of legacy investors. This creates a confounding problem for both small investors and small GPs with a seemingly narrow solution. These LPs need to accept the shifted risk profile even if it means a less-than-proportional change in return expectations. In turn, due diligence will be critical for these investors looking for top-performing managers from an increasingly risky pool of options.