From China to Japan, each market has evolved differently and presents a unique set of opportunities and challenges

From China to Japan, each market has evolved differently and presents a unique set of opportunities and challenges

As the Asia-Pacific private equity industry matures, the secondary market – where buying and selling of assets takes place before a private equity fund’s agreed term is up – is buzzing with activity. Secondary deals data is difficult to track – most market participants are secretive about their motivations – but Preqin data shows that specialized secondary fund strategies are on the rise.

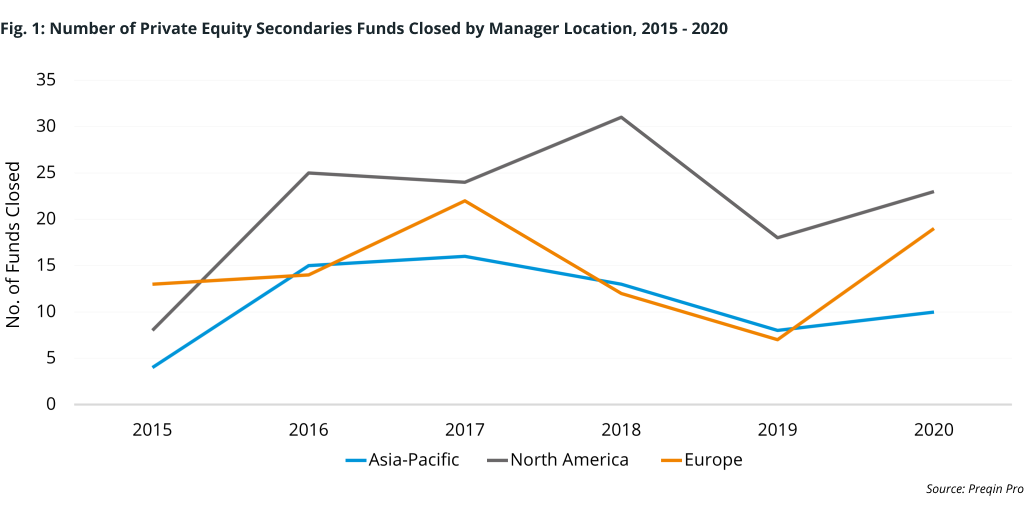

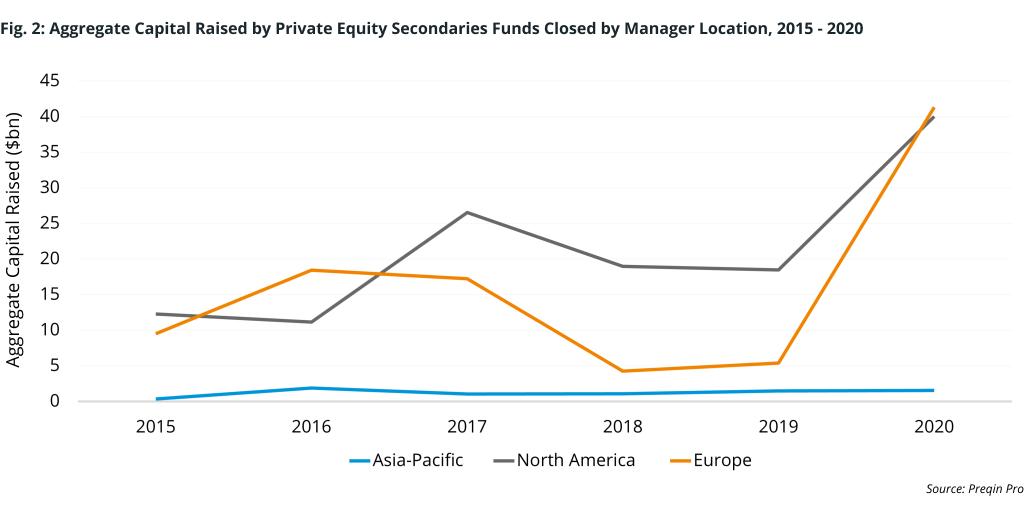

While activity in Asia-Pacific pales in comparison to the more developed markets in the US and Europe, GPs and LPs in the region are increasingly tapping the secondary market for new opportunities and liquidity solutions. In 2020, 10 Asia-Pacific-focused secondaries funds raised a total of $1.6bn, up from $1.5bn raised by eight funds in 2019 (Figs. 1-2). We asked four secondary market experts who’s buying, who’s selling, and what’s driving those decisions.

Alex Lee, Managing Partner at Axiom Asia Private Capital

Historically, most secondary buyers have had a strong preference for buyout funds. In recent years we’ve seen more transactions involving growth and venture capital assets, but these continue to trade at larger discounts than buyout funds.

We have purchased secondaries from a wide variety of sellers in the past year, including a Chinese real estate developer seeking to raise cash, a Southeast Asian conglomerate divesting non-core assets, a Korean venture capital fund approaching the end of its fund life, a Chinese angel investor with liquidity needs, a sovereign wealth fund divesting tail-end assets, and RMB investors in RMB-to-USD fund restructurings.

_________________________________________________________________________________________________

Shinichiro Shiraki, CEO at Aizawa Asset Management Co.

The LP secondaries market in Japan is in a nascent stage. Over the last few decades, only a limited number of institutional investors have allocated capital into global private equity funds. These institutions have occasionally divested their LP positions in the last few years, to clean up their balance sheets. From 2014 to 2018, many employees’ pension funds were liquidated due to legal reform. During that process, those pension funds divested their LP portfolios and created temporary LP secondary opportunities. However, the size and number of LP secondary transactions in Japan remain small and limited, trailing far behind the US and European markets. There are more opportunities to be found in the market for GP-led secondaries, since Japan has a large number of local venture capital funds and many of these have held residual positions even after their funds are dissolved. However, few players choose to acquire equities from those venture capital funds as those positions are mostly unattractive stakes in zombie businesses.

The Japanese secondaries market is different from other markets because most local institutional investors hesitate to divest their LP positions, a process which often forces them to incur realized losses. If they do decide to liquidate their LP positions, they prefer to keep a low profile. Hence, most deals tend to be taken up by a limited pool of credible buyers. Funds also tend to be domiciled in Japan and regulated by Japanese law, so secondary deals are primarily transacted between local financial institutions because the size of most transactions is too small for global buyers to consider for the amount of legal and tax work they have to undertake.

Occasionally, large institutions with allocations to global private equity funds will divest their positions, and these deals can be sized between $100mn and $1bn. Global buyers can access these deals through investment banks and brokers. However, the number of these global transactions is limited.

There are some emerging secondary managers in Japan, and we expect the secondary market will continue to grow gradually. The size and number of private equity investments in Japan has been on the rise since 2015, and secondary market activity should pick up when those private equity funds near their end-of-life. However, there are barriers to entry for global players, such as language, legal, and tax issues, and the Japanese cultural preference for local and closed deals.

_________________________________________________________________________________________________

Vincent Qin, Managing Partner at Shanghe Capital

The rapid growth of private equity investments in China in prior years has created a solid asset base for secondary transactions. Since the 'Innovation and Entrepreneurship’ policy was introduced in the fourth quarter of 2014, the volume of private equity fundraising in China rocketed to RMB 8tn ($1.24tn) during 2015-2020 alone, which accounts for 70% of total funds raised in the past 20 years. Transactions are also being driven by rising liquidity management needs from both LPs and GPs.

There are two main reasons behind a secondary sale in China:

i. The first is policy driven: the ‘New Asset Management Rules’ issued in 2018 require financial institutions and some sovereign funds that were originally major LP investors to cut their private equity investments. They are incentivized to sell their private equity assets, including top-performing fund interests, which is a good source of secondary opportunities.

ii. The second is DPI driven: LPs in China are getting more sophisticated, and as funds of vintage 2014-2015 come to the end of their investment period, distributions to paid-in capital (DPI) has become the center of concern. Both LPs and GPs are starting to turn to the secondary market.

In 2020, we started to see large secondary transactions involving Chinese private equity funds. But outside of the large GP-led transactions, two out of three secondary transactions in China are LP led. The latter are usually transacted in private and seldom publicized. The market still needs time to reach its prime in terms of acceptance and expertise, but the rising supply of both LP- and GP-initiated secondary transactions has nurtured emerging independent secondary fund managers in China on the buy-side.

One difficulty we see is the lack of market-driven capital in the region. Dry powder is mostly supplied by local sovereign funds and they are growing rapidly – accounting for 70-80% of available capital on the market. Chinese pension funds, however, do not invest in private equity. Meanwhile, overseas LPs and GPs are key players in the Chinese secondaries market. As the overseas players are more familiar with secondaries investing, they tend to have more realistic return expectations and a longer investment horizon.

In the early years, secondaries funds were perceived to be less selective about assets, holding mostly tail-end funds in their portfolios. They also had limited market know-how and post-investment service capabilities. Today, compared to developed market funds in the US and Europe, top secondaries funds in China could achieve higher average IRRs given China’s rapid growth, and if they acquire assets with the right timing and vintage.

In this growing market, we see an opportunity to be the first mover, providing unique transaction execution expertise in the region and adding value to portfolio companies, GPs, and LPs in the long run.

_________________________________________________________________________________________________

Zhenlei Huang, Vice General President at Beijing Equity Exchange Center

China's private equity and venture capital (PEVC) secondary shares (S-funds) market is still in a fledgling state, but it is flourishing. At the end of 2020, PEVC funds in China had combined assets under management of over RMB 11tn. Many funds that have expired or are about to expire are struggling with proper exits. This represents a tremendous opportunity for investors in S-funds or S-strategies to purchase some high-growth potential assets at a reasonable discount. While IPOs are still the dominant exit strategy for Chinese PEVC fund managers, exits via S-funds and packaged-asset transactions are a rising trend.

2020 was an important turning point for the market, as COVID-19 triggered sharp asset price corrections and fund withdrawals for many PEVC managers. With most of the incremental liquidity from loose fiscal and monetary policies flowing into the stock market, PEVC managers found it hard to raise new capital. Those with portfolios weighted heavily toward low-liquidity assets, namely equities of early-stage companies, were forced to seek new exit strategies.

2020 was also the year where Beijing committed to opening up and deepening reforms in the services industry, through the inception of the ‘Two Zones’ of Beijing's National Comprehensive Demonstration Zone for Expanding Opening-up of the Service Sector and the Free Trade Pilot Zone. Building up China’s private equity market and facilitating more cross-border capital flows is a key focus of the Two Zones plan. Coller Capital’s establishment of a secondary fund in Chaoyang, Beijing, has attracted plenty of attention. However, this solution is imperfect – there is no systematic way to approach buyers and sellers, and transactions are not done in a systematic way, which results in lower transaction efficiency.

It is noteworthy that regulators have recognized risks and problems embedded in S-share transactions. As part of the Two Zones initiative, the Beijing Equity Exchange Center (BJOTC), also known as the New Fourth Board, was tasked to build an OTC (over-the-counter) platform for secondary transactions and given the role of regulating transactions and improving the ecosystem. BJOTC strives to solve the problem of information asymmetry in the secondary market by attracting more buyers and sellers onto our platform, in order to create a two-sided network effect. BJOTC utilizes a blockchain-based trading system to guarantee the immutability of transaction records and enhance the trust between transaction partners. Over time, BJOTC seeks to use the accumulated transaction data to develop preliminary valuation tools, which can be used to improve price discovery.