The US pension system appears to have found its sweet spot when it comes to alternatives, but a deeper look shows that plans are divided on where, and with whom, they put their money

The US pension system appears to have found its sweet spot when it comes to alternatives, but a deeper look shows that plans are divided on where, and with whom, they put their money

The Global Financial Crisis (GFC) marked a sea change for the US public pension system. The combination of massive asset drawdowns and falling interest rates dealt significant blows to both assets and liabilities, ushering in a new reality. In this environment, returns moved into the spotlight and the pension system ramped up its alternatives programs, from an average allocation of 15% of total assets in 2007 to nearly 31% at the end of 2020 (Fig. 1). What followed was a $1tn influx of cash into private capital funds. Now, with many pension plans having reached the logistical limits of their liquidity capacity, this momentum appears to have slowed.

Much of the post-GFC enthusiasm in alternatives began to wane after 2013; rising public equity markets made private capital fees harder to swallow, and liquidity was also a key factor. Without the luxury of endowment-sized investment horizons, many public pensions reached the limit of how much capital they could keep locked up in long-term investment vehicles. Some of these plans, after all, have multibillion-dollar liabilities with significant monthly outflows – something that doesn’t ebb away in choppy markets.

However, not all allocators are created equal. Features like plan size (total assets) and funded status (the ratio of assets to liabilities) segment the public pension fund universe. And these factors are not mutually exclusive: large-asset owners can be in poor or good health, likewise for smaller plans.

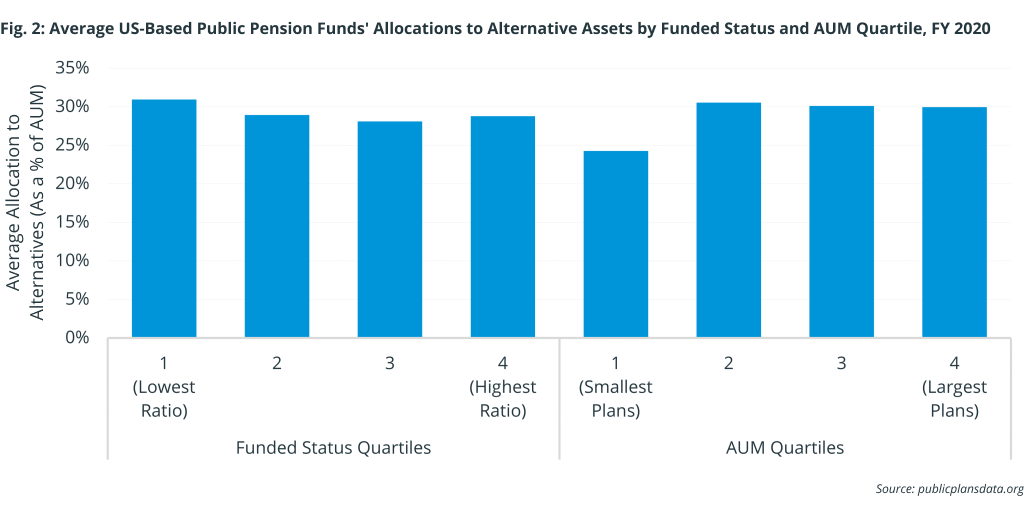

So, to what extent do private capital allocations vary by plan size or funded status? To find out, we divided US public pension plans into quartiles based on both assets and funded status (Fig. 2). While some variance can be seen in the average alternatives allocations across the segments, there’s no statistical significance in the allocations between the groups. In short, the idea that poorly funded plans shot for the moon, allocating more to private capital to get themselves back into better health, or that larger plans committed more freely, isn’t grounded in data.

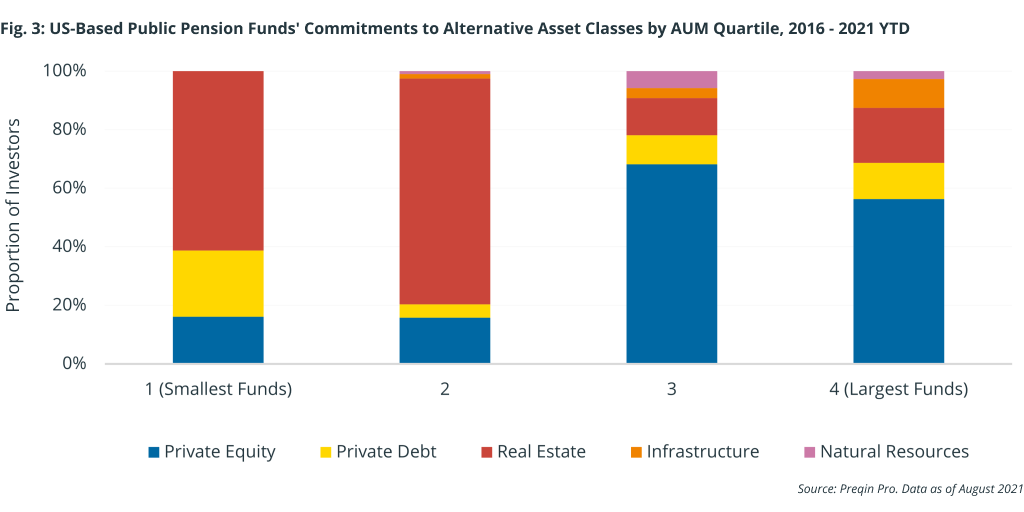

What we did find, however, was that some quartiles invested more capital in some asset classes than others, as Fig. 3 shows. Larger plans, or those above $2.4bn in net assets, and managers in the next-largest quartile had far larger allocations to private equity than those below the median AUM of $400mn.

Additionally, the managers that top-quartile funds invested with are some of the titans of the private capital industry – and they have invested almost exclusively with these firms. The likes of Blackstone, KKR, TPG, and Carlyle, as well as Brookfield’s massive infrastructure fund, are among the most hired private capital managers by total US public pension fund commitments since 2016.

For smaller managers, in contrast, the story is mirrored in their real estate allocations. Pension plans below the asset median have made about 70% of their private capital commitments to real estate since 2016. Additionally, the smallest group (those in the first quartile) have invested more capital in private debt compared with those in the three larger quartiles.

This apparent divide exposes not only the risks associated with a plan’s size, but also its access to the top managers. There are always exceptions to the rule, but regardless of plan size, selectiveness in the alternatives industry goes both ways: GPs choose who they work with as much as LPs choose who they invest with. While this concept is nothing new, the stable state of US pension fund alternatives allocations shows that plans are diverging in strategy and approach. This segmentation is likely to continue, as both the rising demand for private capital exposure and ongoing industry consolidation will cater to those capable of making larger commitments.